10-K: Annual report pursuant to Section 13 and 15(d)

Published on September 23, 2024

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2024

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-42149

Tamboran Resources Corporation

(Exact name of Registrant as specified in its Charter)

| Delaware | 93-4111196 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

| Suite 01, Level 39, Tower One, International Towers Sydney 100 Barangaroo Avenue, Barangaroo NSW |

2000 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrants telephone number, including area code: Australia +61 2 8330 6626

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange |

||

| Common Stock, $0.001 par value | TBN | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of large accelerated filer, accelerated filer, smaller reporting company, and emerging growth company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its managements assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrants executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The registrant was not a public company as of the last business day of its most recently completed second fiscal quarter and, therefore, cannot calculate the aggregate market value of its voting and non-voting common equity held by non-affiliates as of such date.

As of September 20, 2024, the number of shares outstanding of the registrants common stock was 14,224,274.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Tamboran Resources Corporation Proxy Statement for the Annual Meeting of stockholders to be held November 4, 2024 (2024 Proxy Statement) are incorporated by reference into Part III hereof.

Table of Contents

i

Table of Contents

Throughout this Annual Report on Form 10-K (or this report), the following company or industry specific terms and abbreviations are used:

analogous reservoir refers to analogous reservoirs, as used in resources assessments, having similar rock and fluid properties, reservoir conditions (depth, temperature and pressure) and drive mechanisms, but are typically at a more advanced stage of development than the reservoir of interest and thus may provide concepts to assist in the interpretation of more limited data and estimation of recovery. When used to support proved reserves, an analogous reservoir refers to a reservoir that shares the following characteristics with the reservoir of interest: (i) same geological formation (but not necessarily in pressure communication with the reservoir of interest); (ii) same environment of deposition; (iii) similar geological structure; and (iv) same drive mechanism.

appraisal well refers to a vertical or horizontal well designed to assess the properties of the prospective formation by performing open hole logging activities, diagnostic fracture injection testing, fracture stimulation, flow testing, or any combination of the above for the purpose of formation evaluation. Our use of the term appraisal well correlates to the term exploratory well as defined in Rule 4-10(a) of Regulation S-X.

ASX refers to the Australian Securities Exchange.

Beetaloo refers to the Beetaloo Basin of the Northern Territory, Australia.

Beetaloo Joint Venture refers to the unincorporated joint venture in respect to EPs 76, 98 and 117, between TB1 Operator (77.5% working interest) and Falcon (22.5% non-operated working interest).

Bcf refers to one billion cubic feet.

Bcf/d refers to one billion cubic feet per day.

bp refers to BP Singapore Pte. Ltd, a subsidiary of BP plc.

Btu refers to British thermal unit, which is the heat required to raise the temperature of one pound of liquid water by one degree Fahrenheit.

CDI refers to a CHESS Depository Interest.

CO2 refers to carbon dioxide.

CO2-e refers to carbon dioxide equivalent.

completion refers to the installation of permanent equipment for production of oil or gas.

Corporate Reorganization refers to the transactions pursuant to which, among other things, we (i) issued to eligible shareholders of TR Ltd. one CDI of our common stock for every one ordinary share of TR Ltd., in each case, as held on the scheme record date, (ii) amended the terms of each of the outstanding options to acquire ordinary shares of TR Ltd. so that the entitlements of option holders to be issued ordinary shares in TR Ltd. instead became entitlements to be issued CDIs in the Company, (iii) maintained an ASX listing for our CDIs, with each CDI representing 1/200th of a share of our common stock, (iv) delisted TR Ltd.s ordinary shares from the ASX, and (v) became the parent company to TR Ltd.

Corporations Act refers to the Australian Corporations Act, 2001 (Cth).

ii

Table of Contents

Daly Waters or DWE refers to Daly Waters Energy, LP, which is 100% owned by Formentera Australia Fund, LP, which is managed by Formentera Partners, LP, a private equity firm of which Bryan Sheffield serves as managing partner.

Daly Waters Placement refers to the intended issuance at the closing of the offering of $7.5 million in shares of our common stock at the initial public offering price to Daly Waters, or its nominee, in satisfaction of certain payment obligations under the TB1 Joint Venture Agreement. See Business and PropertiesAgreements Relating to the Development of our Assets.

Daly Waters Royalty refers to Daly Waters Royalty, LP.

developed acres refers to the number of acres that are allocated or assignable to productive wells.

development well refers to a well drilled within the proved area of an oil or gas reservoir to the depth of a stratigraphic horizon known to be productive.

drilling space unit or DSU refers to the area allocated to a well for the purpose of drilling for or producing oil or gas.

ESG refers to environmental, social and governance.

estimated ultimate recovery or EUR refers to the sum of reserves remaining as of a given date and cumulative production as of that date.

exploratory well refers to a well drilled to find or establish a new productive oil or natural gas reservoir, or to delineate the extent of a known productive reservoir.

extension well refers to a well drilled in an effort to extend the limits of a known productive reservoir.

farmin agreement refers to an agreement under which the owner of a working interest in license assigns the working interest or a portion of the working interest to another party (the farmee) as a means to share the costs and risks of development. Generally, the farmee agrees to pay the cost of the working interest owner (the farmor) to drill one or more wells. As consideration for the farmees services, the farmor transfers to the farmee a portion of the farmors interest in the license.

Falcon or FOG refers to Falcon Oil and Gas Australia Ltd, a wholly owned subsidiary of Falcon Oil and Gas Limited (TSX.V: FOG, London AIM: FO).

Australian Federal Government refers to the federal government of Australia.

frac refers to the drilling method for extracting oil and natural gas.

GAAP refers to generally accepted accounting principles in the United States.

GHG refers to greenhouse gases.

gross acres or gross wells refers to the total acres or wells, as the case may be, in which a working interest is owned.

H&P refers to Helmerich & Payne International Holdings, LLC, a subsidiary of Helmerich and Payne, Inc. (NYSE: HP).

iii

Table of Contents

Henry Hub refers to a natural gas pipeline located in Erath, Louisiana that serves as the official delivery location for futures contracts on the NYMEX. The settlement prices at the Henry Hub are used as benchmarks for the North American natural gas market.

IP30 refers to 30-day initial production.

IP60 refers to 60-day initial production.

IP90 refers to 90-day initial production.

Mcf refers to one thousand cubic feet.

MMBtu refers to one million Btus.

MMcf/d refers to one million cubic feet per day.

Mtpa refers to million metric tons per year.

net acres refers to the gross acres on which an owner holds an interest, proportionally reduced by the working interest in such acreage. For example, an owner who has 50% interest in 100 acres owns 50 net acres.

net wells refers to the gross wells on which an owner holds an interest, proportionally reduced by the working interest in such wells. For example, an owner who has 50% interest in 100 wells owns 50 net wells.

net zero equity refers to the elimination and/or offset of GHG emissions, on an equity share basis, for the relevant emission scopes referred to.

Northern Territory refers to the Northern Territory of Australia.

operational net zero refers to the full elimination and/or offset of Scope 1 and Scope 2 emissions in our upstream businesses, based on an equity share approach.

Origin Energy refers to Origin Energy Limited (ASX: ORG).

Origin Retail refers to Origin Energy Retail Pty Ltd., a subsidiary of Origin Energy.

ORRI refers to overriding royalty interest.

petrophysical analysis refers to the integration and analysis of various data types, including well logs, core samples and fluid samples and comparison of data with other relevant geological and geophysical information to describe the reservoir properties.

Petroleum Act refers to the Petroleum Act 1984 (NT).

probable reserves refers to additional reserves that are less certain to be recognized than proved reserves but which, together with proved reserves, are as likely as not to be recovered.

productive well refers to an exploratory, development, or extension well that is capable of producing either oil or gas in sufficient quantities to justify completion as an oil or gas well.

prospective resources refers to quantities of oil and gas estimated to exist in naturally occurring accumulations. A portion of the resources may be estimated to be recoverable, and another portion may be considered to be unrecoverable. Resources include both discovered and undiscovered accumulations.

proved reserves refers to quantities of oil, natural gas and NGLs that, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible-from a given date

iv

Table of Contents

forward, from known reservoirs, and under existing economic conditions, operating methods and government regulations-prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or we must be reasonably certain that it will commence within a reasonable time. For a complete definition of proved crude oil and natural gas reserves, refer to the SECs Regulation S-X, Rule 4-10(a)(22).

reserves refer to estimated remaining quantities of oil and gas and related substances anticipated to be economically producible, as of a given date, by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and gas or related substances to market, and all permits and financing required to implement the project.

resources refers to quantities of oil and gas estimated to exist in naturally occurring accumulations. A portion of the resources may be estimated to be recoverable, and another portion may be considered to be unrecoverable. Resources include both discovered and undiscovered accumulations.

royalty interest refers to an interest in an oil and natural gas lease that gives the owner of the interest the right to receive a portion of the production from the leased acreage (or of the proceeds of the sale thereof), but generally does not require the owner to pay any portion of the costs of drilling or operating the wells on the leased acreage. Royalties may be either landowners royalties, which are reserved by the owner of the leased acreage at the time the lease is granted, or overriding royalties, which are usually reserved by an owner of the leasehold in connection with a transfer to a subsequent owner.

Santos or Santos QNT refers to Santos QNT Pty Ltd, a wholly owned subsidiary of Santos Ltd (ASX: STO).

scheme of arrangement refers to a statutory scheme of arrangement under Australian law under Part 5.1 of the Corporations Act.

Scope 1 emissions refers to direct GHG emissions that occur from sources that are controlled or owned by an organization.

Scope 2 emissions refers to indirect GHG emissions associated with the purchase of electricity, steam, heat or cooling.

Scope 3 emissions refers to GHG emissions that result from the end use of an organizations products, as well as emissions from other business activities from assets not owned or controlled by the organization but that the organization indirectly impacts in its value chain.

Shell refers to Shell Eastern Trading (Pte) Ltd, a subsidiary of Shell plc (NYSE: SHEL).

Tamboran refers to Tamboran Resources Corporation, a Delaware corporation.

TB1 refers to Tamboran (B1) Pty Ltd, an Australian private limited company, which is a 50 / 50 joint venture between us and Daly Waters that holds a 77.5% working interest in the Beetaloo Joint Venture through its wholly owned subsidiary, TB1 Operator.

TB1 Operator refers to Tamboran B2 Pty Ltd, an Australian private limited company.

TR Ltd. refers to Tamboran Resources Pty Ltd (f/k/a Tamboran Resources Limited), an Australian private limited company and wholly owned subsidiary of Tamboran following the Corporate Reorganization.

v

Table of Contents

TR West refers to Tamboran (West) Pty Ltd, an Australian private limited company.

unconventional drilling refers to the application of advanced technology, other than traditional vertical well extraction, to extract oil and natural gas resources. Unconventional drilling typically includes directional drilling across long, lateral intervals within narrow horizontal formations offering greater contact area with the producing formation, and various types of hydraulic fracturing at multiple stages to optimize production.

unconventional natural gas refers to natural gas that cannot be produced at economic flow rates nor in economic volumes unless the well is stimulated by a hydraulic fracture treatment, a horizontal wellbore, or by using multilateral wellbores or some other technique to expose more of the reservoir to the wellbore.

unconventional play refers to a set of known or postulated oil and or natural gas resources or reserves warranting further exploration which are extracted from (a) low-permeability sandstone and shale formations and (b) coalbed methane. These plays require the application of unconventional drilling to extract the oil and natural gas resources.

unconventional resources refers to the umbrella term for oil and natural gas that is produced by means that do not meet the criteria for conventional production. What has qualified as unconventional at any particular time is a complex function of resource characteristics, the available exploration and production technologies, the economic environment, and the scale, frequency and duration of production from the resource. The term is most commonly used in reference to oil and gas resources whose porosity, permeability, fluid trapping mechanism, or other characteristics differ from conventional sandstone and carbonate reservoirs. Coalbed methane, gas hydrates, shale gas, shale oil, fractured reservoirs and tight gas sands are considered unconventional resources.

undeveloped acre refers to acreage on which wells have not been drilled or completed to a point that would permit the production of economic quantities of crude oil, NGLs, and natural gas, regardless of whether such acreage contains proved reserves. Undeveloped acres include net acres held by operations until a productive well is established in the spacing unit.

unproved properties refers to properties with no proved reserves.

working interest refers to the right granted to the lessee of a property to explore for and to produce and own natural gas or other minerals. The working interest owners bear the exploration, development, and operating costs on either a cash, penalty, or carried basis.

vi

Table of Contents

Trademarks and Trade Names

This report contains, and incorporates by reference, references to trademarks, service marks and trade names belonging to us or other entities. All trademarks, service marks and trade names included or incorporated by reference into this report are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this report or the documents incorporated by reference herein, including logos, artwork and other visual displays, may appear without the ® or symbols, but such references are not intended to indicate, in any way, that the respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

Cautionary Note Regarding Industry and Market Data

This report includes information concerning our industry and the markets in which we will operate that is based on information from various sources including public filings, internal company sources, various third-party sources and management estimates. Our management estimates regarding our position, share and industry size are derived from publicly available information and its internal research, and are based on a number of key assumptions made upon reviewing such data and our knowledge of such industry and markets, which we believe to be reasonable. While we believe the industry, market and competitive position data included in this report is reliable and is based on reasonable assumptions, such data is necessarily subject to a high degree of uncertainty and risk and is subject to change due to a variety of factors, including those described in Cautionary Note Regarding Forward-Looking Statements, Summary Risk Factors, Risk Factors and elsewhere in this report. These and other factors could cause results to differ materially from those expressed in the estimates included herein. We have not independently verified any data obtained from third-party sources and cannot assure you of the accuracy or completeness of such data.

Presentation of Financial and Operating Data

Our fiscal year ends on June 30. Unless otherwise noted, any reference to a year preceded by the words fiscal year refers to the twelve months ended June 30 of that year. For example, references to fiscal year 2024 refer to the twelve months ended June 30, 2024. References to dollars, $, U.S. dollars and US$ refer to United States dollars; and references to Australian dollars and A$ refer to Australian dollars.

Tamboran was incorporated on October 3, 2023 and does not have financial operating results prior to the Corporate Reorganization effective December 13, 2023. As a result of the Corporate Reorganization, Tamboran became the parent company of TR Ltd., and for financial reporting purposes, the financial statements of TR Ltd. became the financial statements of Tamboran. As a result of the Corporate Reorganization, Tamboran issued to eligible shareholders of TR Ltd. one CDI of its common stock for every one ordinary share of TR Ltd., with each CDI representing 1/200th of a share of Tamborans common stock. Our historical financial statements in this report are presented as though the Corporate Reorganization had taken place on July 1, 2021 and Tamboran had existed as the parent of TR Ltd. as of that date. All share and per share data presented in this report have been retroactively adjusted to reflect a one for two hundred (1:200) exchange ratio and all options over ordinary shares in the predecessor have been retroactively presented as options over CDIs in Tamboran. See Business and PropertiesGeneral Development of Business and Corporate Reorganization.

Rounding and Percentages

The financial information and certain other information presented in this report have been rounded to the nearest whole number or the nearest decimal. Therefore, the sum of the numbers in a column may not conform

vii

Table of Contents

exactly to the total figure given for that column in certain tables in this report. In addition, certain percentages presented in this report reflect calculations based upon the underlying information prior to rounding and, accordingly, may not conform exactly to the percentages that would be derived if the relevant calculations were based upon the rounded numbers or may not sum due to rounding.

Currency Exchange Rate Data

Our functional currency is the Australian dollar, and our consolidated financial statements are presented in the U.S. dollar. The functional currency is the currency of the primary economic environment in which an entitys operations are conducted. We translate our consolidated financial statements into the presentation currency using exchange rates in effect on the relevant balance sheet date for assets and liabilities and average exchange rates for the period for statement of operations accounts, with the difference recognized as a separate component of stockholders equity.

The following exchange rates were used to translate our consolidated financial statements and other financial and operational data shown in constant currency:

| Average for the Fiscal Year |

||||||||

| 2024 | 2023 | |||||||

| A$1.00 |

$ | 0.66 | $ | 0.67 | ||||

Cautionary Note Regarding Emerging Growth Company Status

Section 102(b)(1) of the Jumpstart Our Business Startups Act (JOBS Act) exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard, until such time we are no longer considered to be an emerging growth company. At times, we may elect to adopt a new or revised standard early.

viii

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Forward-looking statements can be identified by words such as: anticipate, intend, plan, goal, commit, seek, believe, project, estimate, expect, strategy, future, likely, may, should, will and similar references to future periods.

It is possible that the Companys future financial performance may differ from expectations due to a variety of factors, including but not limited to: our early stage of development with no material revenue expected until 2026 and our limited operating history; the substantial additional capital required for our business plan, which we may be unable to raise on acceptable terms; our strategy to deliver natural gas to the Australian East Coast and select Asian markets being contingent upon constructing additional pipeline capacity, which may not be secured; the absence of proved reserves and the risk that our drilling may not yield natural gas in commercial quantities or quality; the speculative nature of drilling activities, which involve significant costs and may not result in discoveries or additions to our future production or reserves; the challenges associated with importing U.S. practices and technology to the Northern Territory, which could affect our operations and growth due to limited local experience; the critical need for timely access to appropriate equipment and infrastructure, which may impact our market access and business plan execution; the operational complexities and inherent risks of drilling, completions, workover, and hydraulic fracturing operations that could adversely affect our business; the volatility of natural gas prices and its potential adverse effect on our financial condition and operations; the risks of construction delays, cost overruns, and negative effects on our financial and operational performance associated with midstream projects; the potential fundamental impact on our business if our assessments of the Beetaloo are materially inaccurate; the concentration of all our assets and operations in the Beetaloo, making us susceptible to region-specific risks; the substantial doubt raised by our recurring operational losses, negative cash flows, and cumulative net losses about our ability to continue as a going concern; complex laws and regulations that could affect our operational costs and feasibility or lead to significant liabilities; community opposition that could result in costly delays and impede our ability to obtain necessary government approvals; exploration and development activities in the Beetaloo that may lead to legal disputes, operational disruptions, and reputational damage due to native title and heritage issues; the requirement to produce natural gas on a Scope 1 net zero basis upon commencement of commercial production, with internal goals for operational net zero, which may increase our production costs; the increased attention to ESG matters and environmental conservation measures that could adversely impact our business operations; risks related to our corporate structure; risks related to our common stock and CDIs; and the other risk factors discussed in the this report and the Companys filings with the Securities and Exchange Commission (the SEC).

It is not possible to foresee or identify all such factors. Any forward-looking statements in this report are based on certain assumptions and analyses made by the Company in light of its experience and perception of historical trends, current conditions, expected future developments, and other factors it believes are appropriate in the circumstances. Forward-looking statements are not a guarantee of future performance and actual results or developments may differ materially from expectations. While the Company continually reviews trends and uncertainties affecting the Companys results of operations and financial condition, the Company does not assume any obligation to update or supplement any particular forward-looking statements contained in this report, except as required by law.

Additionally, certain forward-looking and other statements in this Annual Report on Form 10-K or other locations, such as the Companys corporate website, regarding ESG matters are informed by various ESG standards and frameworks (which may include standards for the measurement of underlying data) and the interests of various stakeholders. Accordingly, such information may not be, and should not be interpreted as necessarily being material under the federal securities laws for SEC reporting purposes, even if the Company

1

Table of Contents

uses the word material or materiality in such discussions. ESG information is also often reliant on third-party information or methodologies that are subject to evolving expectations and best practices, and the Companys approach to and discussion of these matters may continue to evolve as well. For example, the Companys disclosures may change due to revisions in framework requirements, availability of information, changes in its business or applicable governmental policies, or other factors, some of which may be beyond its control.

2

Table of Contents

The following is a summary of the material risks and uncertainties we have identified, which should be read in conjunction with the more detailed description of each risk factor contained below.

Risks Related to Our Business and Industry

| | We are an early stage development company with no material revenue expected until 2026, at the earliest. We have a limited operating history, and our future performance is uncertain. Our ability to successfully drill and complete the wells identified for our current capital plan will depend on a variety of factors; |

| | Our business plan requires substantial additional capital, which we may be unable to raise on acceptable terms in the future, or at all, which may in turn limit our ability to execute on our plans; |

| | Our business plan contemplates delivering natural gas to the Northern Territory, the Australian East Coast, as well as select markets in South and East Asia. Our ability to deliver natural gas in significant quantities to these markets depends on the construction of additional pipeline capacity. We cannot assure you that we will be able to secure sufficient take-away capacity on our timing or at all; |

| | We have no proved reserves at this time and areas that we decide to drill may not yield natural gas in commercial quantities or quality, or at all; |

| | Drilling wells is speculative, often involving significant costs that may be more than our estimates, and may not result in any discoveries or additions to our future production or reserves. Any material inaccuracies in drilling costs, estimates or underlying assumptions will materially affect our business; |

| | We intend to import and implement U.S. practices and technology for use in the development of our properties in the Northern Territory. There is limited experience with these practices and technology within the workforce in the areas we operate. The ability to attract and train a qualified workforce could hamper our present operations and limit our ability to grow; |

| | Our inability to access appropriate equipment and infrastructure in a timely manner may hinder our access to natural gas markets and delay the phases of our business plan; |

| | Drilling, completions, workover and hydraulic fracturing operations are operationally complex activities which present certain risks that could adversely affect our business, financial condition or results of operations; |

| | Natural gas prices are volatile. A reduction or sustained decline in prices may adversely affect our business, financial condition or results of operations and our ability to meet our financial commitments or raise capital; |

| | Construction of midstream projects subjects us to risks of construction delays, cost over-runs, limitations on our growth and negative effects on our financial condition, results of operations, cash flows and liquidity; |

| | If our assessments of the Beetaloo are materially inaccurate, it will have a fundamental impact on our business; |

| | All of our assets and operations are located in the Beetaloo, making us vulnerable to risks associated with operating in one geographic area; and |

| | Our recurring losses from operations, negative cash flows and substantial cumulative net losses raise substantial doubt about our ability to continue as a going concern. |

Risks Related to Environmental, Legal Compliance and Regulatory Matters

| | We are subject to complex federal, local and other laws and regulations that could adversely affect the cost, manner or feasibility of conducting our operations or expose us to significant liabilities; |

3

Table of Contents

| | We face community opposition from certain parties with respect to our development of the Beetaloo and related operations, which could result in significant costs and delays and could impede our ability to obtain the government approvals required for such operations; |

| | The exploration and development of natural gas in the Beetaloo can pose native title and heritage risks, potentially leading to legal disputes, operational disruptions, and reputational damage; |

| | Upon commencement of commercial production, we are required by the Australian government to produce natural gas in the Beetaloo on a Scope 1 net zero basis. We also have set an internal goal of producing natural gas with net zero equity Scope 1 and 2 emissions. Meeting these requirements and goals may increase our costs of production, and we may be unable to meet these requirements and goals; and |

| | Increased attention to ESG matters and environmental conservation measures may adversely impact our business. |

Risks Related to our Corporate Structure

| | We are a holding company. Our sole material asset is our equity interest in TR Ltd. and we will be accordingly dependent upon distributions from TR Ltd. to pay taxes and cover our corporate and other overhead expenses. |

Risks Related to our Common Stock and our CDIs

| | The requirements of being a public company, including compliance with the reporting requirements of the ASX listing rules and the Exchange Act, may strain our resources, increase our costs and distract management, and we may be unable to comply with these requirements in a timely or cost-effective manner; |

| | Changes in foreign currency exchange rates could materially adversely affect our business, results of operations or financial condition; |

| | We have engaged in transactions with our affiliates and expect to do so in the future. The terms of such transactions and the resolution of any conflicts that may arise may not always be in our or our stockholders best interests; |

| | We have identified a material weakness in our internal control over financial reporting. Any material weakness may cause us to fail to timely and accurately report our financial results or result in a material misstatement of our financial statements; |

| | The different characteristics of the capital markets in Australia and the United States may negatively affect the trading prices of our CDIs and common stock, and may limit our ability to take certain actions typically performed by a U.S. company; |

| | Our ability to raise additional capital may be significantly limited by listing rules of the ASX that limit the amount of common stock that we are permitted to issue without stockholder approval; and |

| | As a result of listing CDIs on the ASX, we are subject to the listing rules of the ASX, which may strain our resources, divert managements attention and affect our ability to manage our business or raise additional capital. |

4

Table of Contents

ITEMS 1 AND 2. BUSINESS AND PROPERTIES

General Development of Business and Corporate Reorganization

Headquartered in Sydney, Australia, we have been engaged in the development of Australian oil and natural gas reserves since our formation in 2009. Since 2014, we have focused our development activities within the Northern Territory.

TR Ltd. completed its initial public offering in Australia in July 2021 and was publicly listed on the ASX under the ticker TBN. Tamboran was incorporated in Delaware on October 3, 2023 for the purpose of effecting a scheme of arrangement under Australian law between Tamboran and TR Ltd., which we refer to as the Corporate Reorganization. On December 13, 2023, Tamboran implemented the Corporate Reorganization and acquired all of the outstanding ordinary shares of TR Ltd. in exchange for 1,716,672,600 CDIs representing beneficial interests in 8,583,363 shares of our common stock, with each CDI representing 1/200th of a share of our common stock. Concurrently, TR Ltd.s ordinary shares were delisted from the ASX, and our CDIs were listed on the ASX. Following the Corporate Reorganization, Tamborans assets consisted primarily of 100% of the ordinary shares of TR Ltd. Tamboran completed its U.S. initial public offering (IPO) in July 2024.

The description of our business included in this report as of the dates and for the periods prior to the Corporate Reorganization reflect the business of TR Ltd., and the description of our business as of the dates and for the periods from and after the Corporate Reorganization reflect the business of Tamboran and its consolidated subsidiaries, in each case unless otherwise expressly stated or the context otherwise requires. The consolidated financial statements and other financial information of Tamboran included in this report reflect the historical financial statements of TR Ltd., as retroactively adjusted to give effect to the Corporate Reorganization.

The terms we, us, our and the Company, as used herein and unless otherwise stated or indicated by context, refer to TR Ltd. and its subsidiaries prior to the Corporate Reorganization and to Tamboran and its subsidiaries after the Corporate Reorganization.

Overview

Tamboran is an early stage, growth-driven independent natural gas exploration and production company focused on an integrated approach to the commercial development of the natural gas resources in the Beetaloo Basin located within the Northern Territory of Australia. We and our working interest partners have exploration permits (EPs) to approximately 4.7 million contiguous gross acres (approximately 1.9 million net acres to Tamboran) and are currently the largest acreage holder in the Beetaloo. We believe natural gas will play a significant role in the transition to cleaner energy and are committed to supporting the global energy transition by developing commercial production of natural gas in the Beetaloo with net zero equity Scope 1 and 2 emissions.

5

Table of Contents

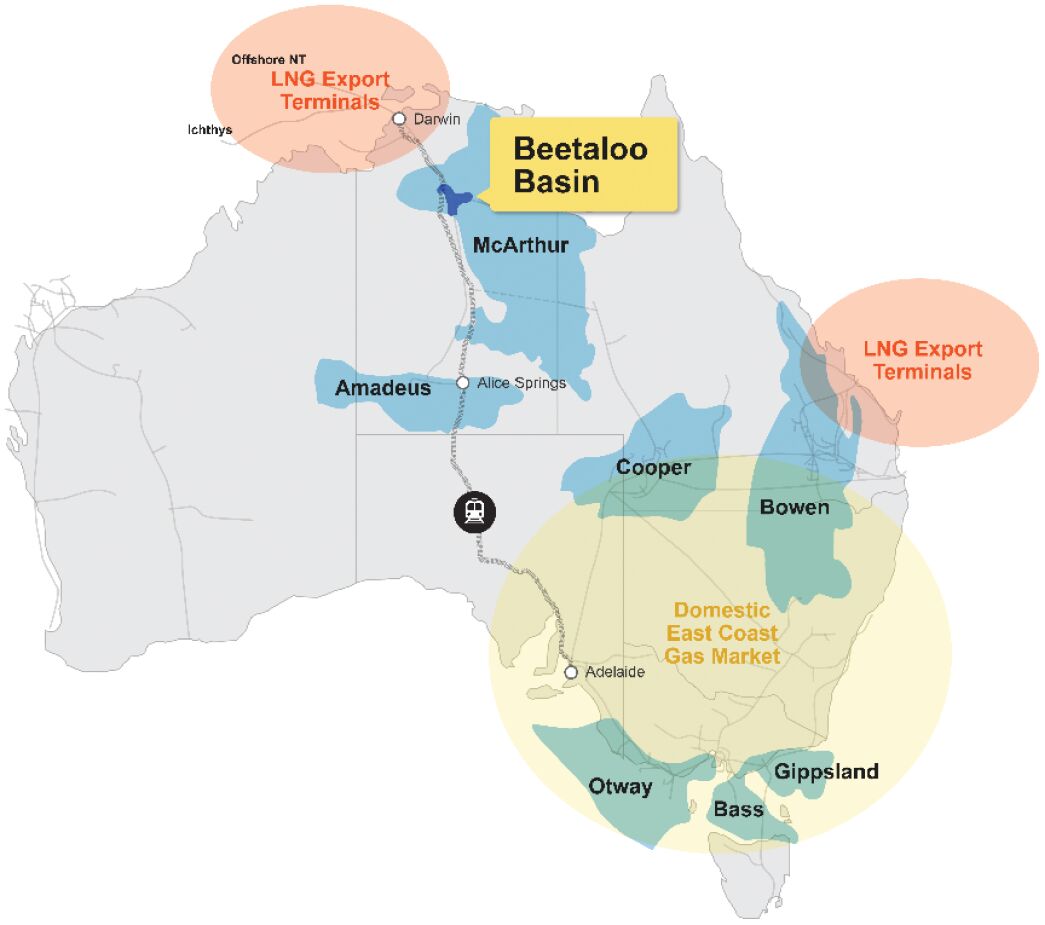

The Beetaloo

The Beetaloo, an area of approximately seven million acres (10,800 square miles), is believed to contain significant quantities of unconventional natural gas resources. The Beetaloo is a structural component of the Greater McArthur Basin in the Northern Territory and is located approximately 300 miles southeast of Darwin, Northern Territory. The following image illustrates the location of the Beetaloo:

Preliminary results and third-party data indicate that natural gas produced in the Beetaloo generally has lower carbon dioxide content compared to natural gas produced elsewhere in Northern Australia and major fields supplying Australias East Coast gas market. We believe our application of U.S. drilling and completion technology will provide us with a competitive advantage to achieve natural gas production in compliance with the Australian governments recently enacted GHG regulations. The Australian governments current policy is to target net zero carbon emissions economy-wide by 2050. Additionally, the Australian government requires all shale gas production in the Beetaloo following commercialization to be conducted on a Scope 1 net zero emissions basis. We have set a target to exceed these requirements by reaching net zero equity Scope 1 and 2 GHG emissions upon commencement of commercial production. We expect there to be a variety of means in which we could achieve our operational net zero goals, including but not limited to, utilizing carbon offsets, for which the prices are capped by applicable law, exploring opportunities to power our facilities with renewable energy sources, implementing methane leakage minimization technology in the design and operation of our production facilities and integrating a carbon capture storage hub with our proposed LNG project.

To date, our appraisal and development activities have focused on the dry gas shale target of the Middle Velkerri B formation, although we expect to eventually evaluate other benches for future development. Regional data from exploration wells, initial results from our appraisal wells, including well log and core data, as well as available 2-D seismic data, indicate that the geological properties of the Middle Velkerri section in the Beetaloo are widespread with geology similar to that of the Marcellus Shale of the Appalachian Basin in the northeastern United States (the Marcellus). In particular, the dry gas areas of the Marcellus qualify as an appropriate analogous reservoir to the Middle Velkerri shale of the Beetaloo, having similar rock and fluid properties (such as organic-rich source rock and similar thermal maturity), similar reservoir conditions (including depth, pressure gradient and temperature ranges), and drive mechanism (using pressure depletion and gas desorption). While the Marcellus is at a more advanced stage of development than the Beetaloo, we believe comparison to the Marcellus may assist in our estimations and interpretation of data.

6

Table of Contents

Our Business Plan

Our business plan consists of three distinct phases in the development of the Beetaloo. The focus of the first phase will be on the transition from exploration activities to the commercialization of our Beetaloo properties. Further to that goal, we expect to:

| | drill and complete an additional two wells in 2024, |

| | four wells in 2025, |

| | progress a project to design and construct the 40 MMcf/d compression and dehydration plant (the Sturt Plateau Compression Facility or SPCF), and |

| | progress a 20-mile pipeline to the existing gas pipeline network (collectively, the Shenandoah South Pilot Project). |

Our goal is to achieve ~40 MMcf/d (gross) plateau production commencing in 1H 2026 from the Shenandoah South Pilot Project. Based on our petrophysical analysis from completed appraisal wells, we have already identified what we believe to be the most productive acreage and shale benches to target for our first stage wells.

We have early development agreements with APA Group (ASX: APA), Australias largest gas infrastructure company by volume whereby APA has committed to the study and planning of a project to build, own, and operate a new 20-mile pipeline to connect our wells to the existing gas transmission network through the Amadeus Gas Pipeline (AGP). Tamboran is progressing the SPCF that would upgrade the raw gas to meet sales gas quality, subject to the terms of definitive development agreements.

We estimate the remaining capital required to deliver the first development phase to production will be approximately $110 million (A$170 million) to $140 million (A$220 million) net to Tamboran (refer to table below).

| A$ millions |

Low | High | ||||||

| Drilling and completions |

100 | 120 | ||||||

| SPCF1 |

20 | 30 | ||||||

| Related pad construction |

20 | 30 | ||||||

| Corporate G&A |

30 | 40 | ||||||

|

|

|

|

|

|||||

| Total 2 |

170 | 220 | ||||||

|

|

|

|

|

|||||

| (1) | Compression facility expenditure assumes new infrastructure partner. Tamboran is evaluating the opportunity to sell interest in the midstream infrastructure asset, with future gas to be tolled via the new third-party infrastructure. |

| (2) | Excludes capital spend on assets outside the Pilot Project area. |

We intend to fund these costs with cash on hand as well as net cash proceeds from one or more debt or equity offerings. We currently expect gas sales to commence from our wells in the first half of 2026. Through the course of the completion of the additional six wells, we believe we can reduce costs through greater efficiency while simultaneously providing us with sufficient data to confirm the EUR for wells drilled in the Beetaloo. Our development plan seeks to efficiently drill from pad wells, utilizing long laterals and modern completion techniques employed by U.S. onshore operators. We expect the cost structure and production profiles achieved with our initial wells to lead to a financial investment decision for an initial large scale drilling program in our second phase.

The second phase of our business plan involves building our drilling program to produce natural gas to supply the Australian East Coast and Northern Territory markets. The existing pipeline infrastructure, the AGP in

7

Table of Contents

the Northern Territory, can export ~50 MMcf/d northbound and ~50 MMcf/d to the East Coast. We have early development agreements with APA whereby APA has committed to the study and planning of a project to construct, own, and operate an approximately 1,000-mile pipeline to connect the Beetaloo to the main trunk line of the East Coast Gas Grid. We anticipate that this pipeline will reduce the cost of transporting gas from the Northern Territory to the East Coast by up to 50%. We have non-binding letters of intent from six of Australias largest energy retailers with respect to the purchase of natural gas from us, with an aggregate volume of 875 MMcf/d for a period of up to 10 to 15 years.

In the third phase of our business plan, following commercialization of the Beetaloo, we intend to drill additional wells with the intent to supply natural gas for export through the existing liquified natural gas (LNG) plants in the Middle Arm Sustainable Development precinct (MASD) Darwin and our proposed 6.6 Mtpa Northern Territory LNG export facility (NTLNG) to South and East Asian markets. Depending on the volume of unused capacity available at existing LNG plants in the MASD Darwin, this phase may occur before or in parallel with the second phase. In consideration of our proposed NTLNG project, the government of the Northern Territory of Australia has awarded us exclusive use of an approximately 420-acre site for a term extending to December 31, 2027 under the Interim Agreement, with two one-year extension options to progress pre-FEED and FEED studies with respect to NTLNG. We completed the Concept Select study in the first quarter of 2024 with Wood Group, which affirmed the feasibility of commencement of commissioning of the first LNG train in 2030. In August 2024, we awarded the EPC contract for pre-FEED activities to Bechtel, the worlds leading LNG EPC contractor. Pre-FEED activities are expected to be completed in 1H 2025.

The MASD, an industrial complex adjacent to the city of Darwin, seeks to provide infrastructure focused on low emissions operations, for the export, processing, storage, shipping and rail transportation of LNG and other hydrocarbons. The MASD precinct is currently home to an export hub with two existing and operational LNG export terminals, the Darwin LNG terminal with a capacity of 3.7 Mtpa and the Ichthys LNG terminal with a capacity of 8.9 Mtpa. The Australian government has committed A$1.5 billion in investments commencing in 2025 to further develop MASD infrastructure and access, including dredging of the deepwater port, construction of road and rail access and distribution of electricity. We estimate total time required for construction of the NTLNG project to be between three to five years and have a non-binding memorandum of understanding with each of BP Singapore Pte. Ltd (bp) and Shell Eastern Trading (Pte) Ltd (Shell) for 20-year LNG purchase contracts. We intend to seek additional strategic partners for the financing and development of these and other infrastructure projects.

Our business and development plans include the continuous focus on reducing costs while increasing production efficiencies. We believe that importing U.S. unconventional drilling and completion techniques, best-practices and technology, together with the right personnel, will reduce the incremental cost to drill and complete each subsequent well. We currently have on contract with Helmerich and Payne, Inc. (NYSE: HP), one H&P FlexRig® with a 10-year option to contract for up to five additional rigs. We have entered into a two-year preferred arrangement with Liberty Energy Inc. (NYSE: LBRT) (Liberty Energy) to provide us dedicated frac fleets and personnel on market terms (as reasonably determined by the Beetaloo Joint Venture).

We estimate the drilling and completion costs of each of the remainder of our initial six wells will average approximately $28 million (gross) as a result of our application of U.S. practices, longer lateral lengths and increased number of stimulated stages. We are targeting long-term development well costs of $16 million per well with horizontal sections of more than 10,000 feet with 60 stages. We believe by taking advantage of efficiencies related to economies of scale, continued infrastructure development in the Beetaloo and resource maturation, over time we will significantly reduce the cost to drill and complete our wells.

8

Table of Contents

Competitive Strengths

We have a number of strengths that we believe will help us successfully execute our business strategy, including:

| | Leading acreage holder and operator in the high-quality Beetaloo. Our Beetaloo assets cover approximately 4.7 million contiguous gross acres (approximately 1.9 million net acres), the most extensive position currently reported in the Beetaloo. Over 5,000 miles of 2-D seismic data has been collected over the Beetaloo. Based on our seismic we believe our acreage position consists of significant quantities of high-quality natural gas resources in what we believe to be the core of the Velkerri shale gas play. Our initial development area of the Middle Velkerri-B shale shows an average shale thickness of 230 feet across approximately 610,400-acres (approximately 950 square miles). We estimate the Middle Velkerri section to be continuous across the same area. The Beetaloo has very few operators and no urban areas. The geographical features of the Beetaloo, our expansive contiguous acreage position and very few restrictive boundaries support more than 10,000-foot laterals and U.S. style unconventional drilling techniques. In addition, we believe our position as the leading acreage holder in the Beetaloo will support our efforts to establish commercial production in volumes sufficient to stimulate investment in in-basin frac sand and other services. |

| | Premium Markets. We expect the relative geographic proximity of the Beetaloo to the major population centers on the Australian East Coast and the Asian LNG markets to provide us the opportunity to potentially obtain attractive prices for our natural gas relative to markets in North America based on historical pricing. For example, during the calendar year 2024 to date, spot prices for natural gas delivered from Henry Hub averaged $2.20 per MMBtu. Over that same period, the Japan Korea Marker (JKM) continuous futures price of LNG averaged $11.23 per MMBtu. Although production costs in the Beetaloo are currently significantly higher than U.S. onshore operations, upon full commercialization of the Beetaloo, we expect those costs to decline. |

| | High caliber and experienced management team with a track record of success. Our senior management team has extensive experience with vertical and horizontal drilling in unconventional plays and an average of over 25 years of experience in the upstream oil and gas industry. Additionally, our leadership team has significant experience managing integrated energy and power assets for large-scale enterprises, including companies such as Unocal, Chevron, Apache, and ExxonMobil. Joel Riddle, our CEO since 2013, has more than 25 years of experience in the upstream oil and gas industry, and Faron Thibodeaux, our COO, has over 40 years of technical and operations experience in the energy industry. Our board of directors includes our Chairman Dick Stoneburner, the former co-founder, President and Chief Operating Officer of Petrohawk Energy Corporation and President North America Shale Production Division for BHP Billiton Petroleum, a subsidiary of BHP Group Ltd. (NYSE: BHP), and Fredrick Barrett, co-founder and former CEO of Bill Barrett Corporation, each of whom have more than 35 years of experience raising capital and operating assets in the oil and gas industry. |

| | Operational Net Zero. Australian law requires that natural gas reserves in the Beetaloo be produced on a Scope 1 net zero basis upon achieving commercial production. We believe we are positioned to achieve net zero equity Scope 1 and Scope 2 emissions (i.e. operational net zero). We have a comprehensive sustainability program, which is overseen and directed by a Sustainability Committee composed of board members. We believe natural gas delivered from the Beetaloo will provide an attractive alternative for domestic and Asian economies seeking to reduce reliance on coal and reduce their own GHG emissions. |

| | High quality, blue-chip strategic partners. We have contracted H&P to exclusively provide drilling services for our wells in the Beetaloo. We have an agreement with Liberty Energy to provide a dedicated frac fleet and personnel. We are working with APA Group to progress access and approvals for a large diameter gas pipeline from the Beetaloo Basin to the Australian East Coast gas grid. In parallel we are working on a pipeline from the Beetaloo Basin to Darwin to deliver gas to our proposed |

9

Table of Contents

| NTLNG facility. Our memoranda of understanding with each of bp and Shell contemplate 20-year LNG purchase agreements from our proposed NTLNG development. We have entered into a gas sales agreement with the Northern Territory Government (NT Government) for gas sales of up to ~40 MMcf/d for a period of up to 15.5 years. We also have non-binding letters of intent from six of Australias largest energy retailers with respect to the purchase of natural gas from us, with an aggregate volume of 875 MMcf/d for a period of up to 10 to 15 years. We are seeking to enter into definitive agreements with these strategic partners as we execute on subsequent phases of our business plan, and we will continue to seek additional strategic partnerships in the development of the Beetaloo. See Agreements Relating to the Development of our Assets in this report and Certain Relationships and Related Person Transactions included in the 2024 Proxy Statement for further information. |

Business Strategies

We intend to execute the following business strategies:

| | Commercialize our resources in the Beetaloo. We intend to commercialize our natural gas resources in the Beetaloo over the next two to three years. Leveraging the experience and data derived from our initial well program, we anticipate commencing a multi-year drilling program as early as 2026, subject to our ability to obtain the necessary capital and completion of certain third-party infrastructure projects, including the proposed pipelines with APA Group. |

| | Pursue an integrated approach to the development and scale of natural gas production and transportation projects. We aim to build additional infrastructure with partners to support the take-away of up to 2.0 Bcf/d of gross production following the initial commercialization of the Beetaloo. Adjacent to the Beetaloo are currently two natural gas pipelines, one running north to Darwin and another pipeline to the Australian East Coast. We are in discussion with APA Group with respect to the construction of a larger diameter pipeline to the Australian East Coast, and we anticipate commencing construction of our NTLNG project as early as 2027, subject to receiving the necessary approvals. Additionally, there are two LNG export terminals in operation near Darwin through which we can eventually sell additional production, subject to capacity constraints. |

| | Import U.S. best practices to become a low-cost provider of natural gas to the Australian domestic market and regional Asian markets. We will continue to import best practices from the U.S. E&P industry to enhance production and reserve recovery per well while simultaneously reducing capital and operating costs. To date, horizontal drilling and completion techniques and pad drilling have not been widely used in the Australian E&P industry. Based on analysis of our preliminary results and seismic data, we believe the geology of the Beetaloo is conducive to U.S.-style unconventional drilling, and we have entered into an agreement with H&P to bring U.S. unconventional drilling rigs to the Beetaloo. We currently have on contract an H&P FlexRig®, which is currently operational within the Beetaloo, with an option to contract for additional rigs. We have an agreement with Liberty Energy to provide a dedicated frac fleet and personnel, which is currently being mobilized to the Beetaloo. |

| | Lower Emissions from Natural Gas Production. As discussed above, we aim to achieve operational net zero from natural gas production. We intend to participate in an open-access, multi-user carbon capture utilization and sequestration project at the proposed NTLNG facility and will seek to power our gathering and processing facilities from renewable sources, including solar and wind, to the extent available. Our goal is to deliver LNG to global markets from net zero equity Scope 1 and 2 operations in an effort to replace coal consumption, particularly in Australian and East Asian markets, with lower-emissions natural gas from the Beetaloo. |

Our Assets and Operations

We currently hold interests in six EPs and one EP(A), all of which are contiguous to one another and located in the Beetaloo. See Title to Properties for further information. Our key assets are (i) a 25% non-operated

10

Table of Contents

working interest in EP 161, (ii) a 38.75% working interest in EPs 76, 98 and 117, where we are the operator, and (iii) a 100% working interest in EPs 136, 143 and EP(A) 197, where we are the operator. The deepest portions of the Beetaloo, and our strategic near-term focus are those areas covered by EPs 76, 98, and 117, which are held indirectly through TB1, a 50/50 joint venture with Daly Waters, an entity controlled by Bryan Sheffield. TB1 holds interests in EPs covering four million gross (1.5 million net) acres. See Agreements Relating to the Development of our Assets TB1 Joint Venture Agreement for a description of the material terms of the TB1 Joint Venture Agreement.

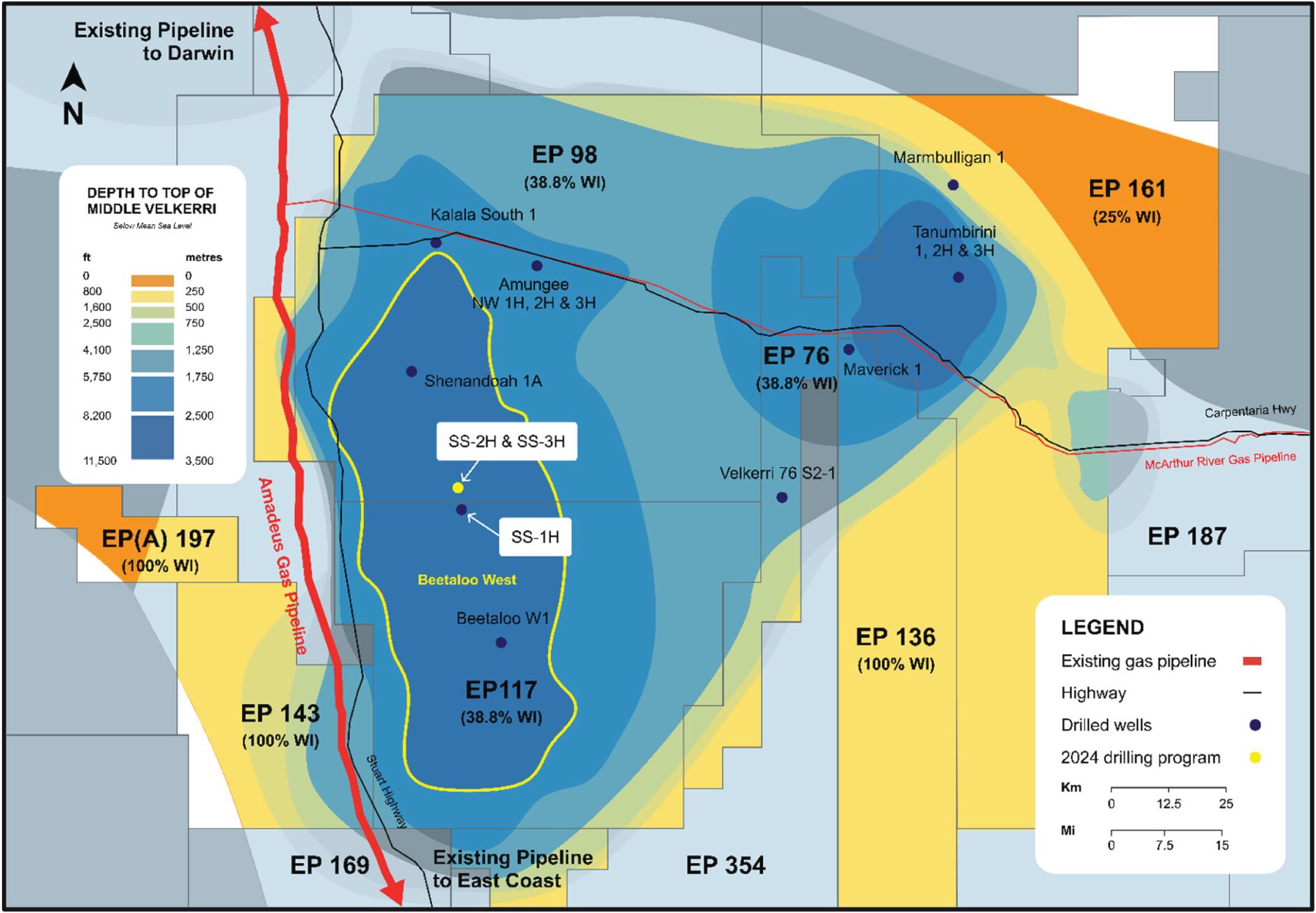

Our assets are depicted by the colored areas in the map of the Beetaloo below, with the deepest core regions of the Beetaloo (the darker blues) in the west being the focus of our development:

Summarized below are our interests, as of June 30, 2024, in exploration permits in Beetaloo Basin together with the wells drilled on such acreage and our associated net working interest. We consider all of our acreage as undeveloped, since even though we classify one of our appraisal wells as productive, acreage has not been allocated or assigned to such well. Our contiguous acreage position and the scarcity of other operators or urban areas near the Beetaloo provide us with the space necessary to eventually drill pad wells with up to three to four-mile horizontal laterals, greatly increasing efficiencies and production from a relatively smaller number of wells.

| Exploration Permit |

Gross / Net Acres | Expiration Date | ||||||

| EP 76 |

346,700 / 134,346 | May 30, 2028 | ||||||

| EP 98 |

2,312,262 / 896,000 | May 30, 2028 | ||||||

| EP 117 |

1,380,864 / 535,085 | May 30, 2028 | ||||||

| EP 136 |

207,000 / 207,000 | July 23, 2029 | ||||||

| EP 143 |

512,000 / 512,000 | March 4, 2028 | ||||||

| EP 161 |

512,000 / 128,000 | March 20, 2026 | ||||||

| EP(A) 197 |

192,000 / 192,000 | N/A | ||||||

11

Table of Contents

As of June 30, 2024, we have participated in six appraisal wells since fiscal year 2021, four of which we drilled as the operator:

| Well, Name1 |

Operator | Non- Operator(s) |

Permit |

Date Drilled | Tamboran Working Interest |

|||||||||||||||

| Tanumbirini #2 (T2H) |

Santos | Tamboran | 161 | May 2021 | 25 | % | ||||||||||||||

| Tanumbirini #3 (T3H) |

Santos | Tamboran | 161 | Aug 2021 | 25 | % | ||||||||||||||

| Maverick 1V (M1V) |

Tamboran | N/A | 136 | Aug 2022 | 100 | % | ||||||||||||||

| Amungee NW-2H (A2H) |

Tamboran | DWE & FOG | 98 | Nov 2022 | 38.75 | % | ||||||||||||||

| Shenandoah South 1H (SS1H) |

Tamboran | DWE & FOG | 117 | Aug 2023 | 38.75 | % | ||||||||||||||

| Amungee NW 3H (A3H) |

Tamboran | DWE & FOG | 98 | Sept 2023 | 38.75 | % | ||||||||||||||

| (1) | Our interests in the A2H, SS1H and A3H are held through a joint venture with DWE, which holds an undivided 77.5% working interest. |

As of June 30, 2024, we operate four gross (approximately 2.2 net) natural gas wells (the SS1H, A2H, A3H, and MIV wells) and hold interests in an additional two gross (approximately 0.5 net) non-operated wells (the T2H and T3H wells). Although none of the wells drilled in the Beetaloo to date are currently flowing to sales, we successfully completed flow testing of our SS1H well and believe it is currently productive. We believe the T2H, T3H, and A2H wells are likely capable of producing sufficient quantities of gas to justify completion or recompletion at a future date with further investment and workover. Our A3H well is capable of being stimulated but is currently drilled but uncompleted. As of June 30, 2024, no additional wells were undergoing or awaiting completion.

In early July 2023, H&Ps FlexRig® that was imported into Australia and successfully mobilized to the SS1H well location targeting the deeper Middle Velkerri B Shale in EP 117. We commenced drilling of the SS1H well in early August 2023 and intersected a 295-foot interval of Middle Velkerri B Shale, the thickest section intersected in the Beetaloo depocenter to date. In February 2024, SS1H delivered an IP30 flow rate of 3.2 MMcf/d over the 1,644-foot, 10-stage stimulated length within the Middle Velkerri B Shale, an IP60 flow rate of 3.0 MMcf/d, and an IP90 flow rate of 2.9 MMcf/d. Normalizing the production rate for a 10,000-foot horizontal lateral, the IP30 flow rate in SS1H would have been approximately 19.5 MMcf/d, the IP60 flow rate would have been approximately 18.4 MMcf/d, and the IP90 flow rate would have been approximately 17.8 MMcf/d.

Also in July 2023, we completed analysis of the T2H and T3H flow tests. The productivity of the wells, which flow tested the Middle Velkerri B Shale at depths of more than 11,000 feet total vertical depth, exhibited higher flowing tubing pressures, thus continuing to validate our internal view that the core deeper areas of the Beetaloo will be more productive and validate further evaluation. Our T2H and T3H well were drilled with low intensity, shorter lateral lengths (approximately 2,000 feet).

In September 2023, we commenced drilling of the A3H well from the same well pad as the A2H well to follow up earlier drilling results. The well was successfully drilled in less than 18 days, the fastest well drilled with a horizontal section in the Beetaloo to date. The activities were completed 20 days faster than the shallower A2H well and approximately 30% lower cost, demonstrating the increased drilling efficiency of the H&P FlexRig®. The A3H well is capable of being stimulated but is currently drilled and uncompleted.

On March 4, 2024, Falcon, the owner of the remaining 22.5% interest in the Beetaloo Joint Ventures assets, capped its participation to 5% in the second Shenandoah South well pad (SS2) and the two wells in the 2024 drilling program. On March 21, 2024, TB1 Operator agreed to pick up Falcons interest, increasing the Companys working interest to at least 47.5% over an area of 51,200 acres around the SS2 well pad. This area is capable of holding up to 23 well pads (or 138 wells with 10,000-foot horizontal sections). and the two wells in the 2024 drilling program. We believe the two DSUs will be more than enough to accommodate all wells associated with the Shenandoah South Pilot Project and over 100 wells for future development phases.

12

Table of Contents

In May 2024, Tamboran received approval of its environmental management plan from the Minister for Environment, Climate Change and Water Security to construct up to four exploration and appraisal sites and undertake drilling and flow testing of up to 15 wells in EP 98 and 117 within the Beetaloo Sub-basin for the Beetaloo Joint Venture.

In late August 2024, we commenced our 2024 Beetaloo Basin drilling activities with the spudding of the SS2H well in the Shenandoah South Pilot Project acreage of EP 98 where Tamboran will hold up to 47.5% working interest following the drilling of the initial two wells. The SS2H and Shenandoah South 3H (SS3H) wells will be drilled from the same well pad with the H&P FlexRig® and will target the Middle Velkerri B Shale at a depth of approximately 9,910 feet (3,020 meters). Both wells are designed to include a 10,000-foot (3,000-meter) horizontal section and will each be stimulated with up to 60 stages utilizing the Liberty Energys modern frac fleet which has recently been mobilized from the US to Australia. Initial flow test results from each well are expected in 1Q 2025. These SS2H and SS3H will create two DSUs totaling 51,200 gross acres around the new SS2 well pad.

Royalty Owners

We will be required to pay a statutory royalty to the NT Government of 10% of the gross value, at the well-head, of all petroleum produced in connection with a production license or EP in a project area. The gross value of that petroleum is determined by the Petroleum Royalty Act (NT). Additionally, we will pay royalties of between 6% to 11% to other third parties under certain commercial arrangements. See Environmental Matters and Regulation and Agreements Relating to the Development of our Assets in this report and Certain Relationships and Related Person Transactions included in the 2024 Proxy Statement for further information.

Mr. Sheffield, our largest shareholder, holds a 2.3% overriding royalty interest (ORRI) through Daly Waters Royalty over all of our Beetaloo assets.

Sweetpea has granted a 4% ORRI in favor of the Tom Dugan Family Limited Partnership, LLP, Territory Oil & Gas, LLC; Malcolm John Gerrard, and Longview of all petroleum produced from the Sweetpea Assets and the land subject to the Sweetpea Assets.

Sweetpea has granted PetroHunter Energy Corporation an ORRI of 2% of the petroleum produced from the land over which the EP 136 and EP 143 were originally granted and EP(A) 197 was applied for.

Sweetpea has granted an undivided 1% ORRI in favor of Jeffrey J Rooney as trustee of the Siegel Dynasty Trust of all petroleum produced from the Sweetpea Assets and the land subject to the Sweetpea Assets. The beneficiaries of the Siegel Dynasty Trust are Emily Siegel and Robert Siegel, who are the children of David N. Siegel, who is a director of Longview and a director of the Company. The ORRI extends to all extensions or renewals of each Sweetpea Assets (as applicable) and to any production licenses or subsequent rights to produce petroleum, from those lands, which are granted or issued to Sweetpea, its successors or assignees.

Middle Arm Development

In July 2024, we were granted an Interim Agreement by the NTG over its 420-acre (170-hectare) site at Middle Arm Sustainable Development Precinct (the Interim MASD Agreement). The Interim MASD Agreement provides us with future exclusivity over the Wirraway North land until the end of 2027 with two 1-year extension periods and maps out how the Crown Lands department will work with Tamboran for future development of the site. The Interim MASD Agreement is expected to be in place until it is replaced by a commercial lease document just prior to FID. We believe the associated infrastructure at MASD provides us the opportunity to initially export up to 6.6 Mtpa through our proposed NTLNG development. We intend to seek

13

Table of Contents

strategic partners in financing and developing the proposed NTLNG development. In June 2023, we announced two non-binding MOUs with bp and Shell to each purchase up to 2.2 Mtpa over a 20-year period from the proposed NTLNG development.

In August 2024, we awarded Bechtel Corporation (Bechtel) pre-FEED studies for the NTLNG development. Bechtel are the worlds leading LNG EPC contractor delivering more than 140 MTPA of LNG (30% of the global LNG production), including nine LNG trains in Australia, with an additional 45 MTPA of capacity currently under EPC, globally. Pre-FEED activities are expected to be completed in 1H 2025 ahead of progression into FEED.

Our Joint Venture Partner

Our largest shareholder is Bryan Sheffield. Mr. Sheffield, through Sheffield Holdings, LP, first began acquiring interests in TR Ltd. in November 2021, has made three subsequent equity investments, and has now grown to become Tamborans largest shareholder, currently holding beneficial ownership of approximately 15.8% of outstanding common stock. Mr. Sheffield has significant investment experience in the U.S. unconventional energy sector. He previously served as the Chairman, CEO and Founder of Parsley Energy Inc., a major independent unconventional oil and gas producer in the Permian Basin in Texas. Parsley Energy was acquired by Pioneer Natural Resources Company in January 2021 for $7.3 billion. He is currently the Managing Partner of Formentera Partners, an energy private equity firm, which has raised $1.2 billion in equity since 2021.

In September 2022, Mr. Sheffield, through Daly Waters, partnered with TR Ltd. through a newly formed 50 / 50 joint venture, TB1, to acquire a 77.5% interest in EPs 76, 98, and 117 covering approximately four million gross acres (1.5 million net acres).

Agreements Relating to the Development of our Assets

TB1 Joint Venture Agreement

We are a member of TB1, a 50/50 joint venture, through our wholly owned subsidiary, TR West, with Daly Waters, an entity controlled by Bryan Sheffield. TB1 in turn wholly owns TB1 Operator. Capitalized terms used but not defined in this section or elsewhere in this report have the meanings ascribed to them in the applicable agreement.

Under the terms of TB1s amended and restated joint venture and shareholders agreement dated June 3, 2024 (the TB1 Joint Venture Agreement), TB1 is governed by a board (the TB1 Board) of not more than six members, with the number of directors appointed by the joint venture parties in respect of their proportion of equity ownership. The parties have no right to designate directors at such time as such partys ownership falls below 10% of the outstanding equity interests in TB1. The TB1 Board currently consists of four board members; two designated by the Company (Joel Riddle and Patrick Elliott) and two designated by Daly Waters (Stephanie Reed and Blake London).

We are the manager of TB1 with responsibility to carry out day to day operations, including managing the activities of the TB1 Operator in operating the properties and complying with the Beetaloo JOA and Falcon Agreement. The manager is also responsible for submitting work plans and budgets with respect to the development of the properties by the TB1 Operator, in accordance with the terms of the Beetaloo JOA, and submitting production and retention licenses. Under the TB1 Joint Venture Agreement, we have agreed to use all reasonable endeavors to apply for a production license for certain permit areas, where justified by appraisal results, by June 30, 2025.

14

Table of Contents

Special Approvals

Under the TB1 Joint Venture Agreement, TB1 is not permitted to take any of the following actions without the affirmative consent of 75% or more of the total number of votes cast by directors present and entitled to vote at a duly convened meeting of the TB1 Board:

| | entering into any partnership or joint venture; |

| | entering into any new borrowing facility in excess of $5 million; |

| | decisions to dispose of or vary the terms of a permit or apply for any new permit; |

| | decisions to proceed to development or production; |

| | sell or otherwise dispose of assets valued at A$5 million or more; |

| | entering into any material agreement with any director, shareholder of any affiliate of the foregoing; |

| | approval of any work program and budget, or any revision of the scope of any approved work program and budget, or approval of variances to any such work program or budget; |

| | approval under the Beetaloo JOA of any authority for expenditure in excess of $250,000; |

| | approval to award any contract for Joint Operations over $250,000; and |

| | all decisions under, or any amendment or variation of, the Gas Sale Agreement between TB1 and Origin Retail dated September 18, 2022 (the Origin GSA). |

In addition, without the prior approval of shareholders holding 75% or more of the total number of votes cast by shareholders present and entitled to vote at a duly convened meeting of the shareholders, TB1 will not take any of the following actions:

| | amendment of the constitution; |

| | loans or financial accommodations with shareholders; |

| | incurring liability under any guarantee or indemnity; |

| | issuing new shares or other securities not contemplated by the TB1 Joint Venture Agreement; |

| | changing the issued share capital; |

| | cessation of or material alteration of the scale of operations; |

| | disposal or encumbering of the shares in a subsidiary; and |

| | seeking an initial public offering on any securities exchange. |

Sole Funding Period

Under the TB1 Joint Venture Agreement, we have agreed to fund TB1s 77.5% working interest in the permits for Operations conducted during the sole funding period, including the cost to drill, multi-stage hydraulic fracture stimulate and flow-test the A2H and SS1H wells for at least 60 days. The sole funding period finalized on March 25, 2024, after completing the flow test of the SS1H well for a total of 60-days. Following the sole funding period, each of the joint venture parties is required to fund its respective equity share of working capital costs in proportion with its equity interest in TB1, in accordance with the cash call schedule described in an approved work program and budget.

Cash Call and Dilution

If a party fails to make a required cash call, the other party may elect to make the contribution on such defaulting partys behalf and cause the contributed amount to constitute debt owing from the non-contribution

15

Table of Contents

party bearing interest at consistent with the Agreed Interest Rate defined in the Beetaloo JOA, defined generally as average quote rate for 90-day Australian bills of exchange plus 4%. Alternately, a party may make the contribution on such defaulting partys behalf and cause the contributed amount to constitute additional equity, receiving additional shares in TB1 at a value of A$1.00 per share.

Technical Committee