EX-99.1

Published on September 20, 2024

Exhibit 99.1 NYSE: TBN, ASX: TBN FY24 Result Presentation Joel Riddle – Managing Director and Chief Executive Officer September 20, 2024 SHENANDOAH SOUTH 2 WELLPAD, NORTHERN TERRITORY, AUSTRALIA

Disclaimer The information in this presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which include statements on Tamboran Resources Corporation's ( we , us or the Company ) opinions, expectations, beliefs, plans objectives, assumptions or projections regarding future events or future results. All statements, other than statements of historical fact included in this presentation regarding our strategy, present and future operations, financial position, estimated revenues and losses, projected costs, estimated reserves, prospects, plans and objectives of management are forward-looking statements. When used in this presentation, words such as “may,” “assume,” “forecast,” “could,” “should,” “will,” “plan,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “budget”, achieve, progress, target, expand, deliver“, potential, propose, enter, provide, contribute, and similar expressions are used to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current belief, based on currently available information, as to the outcome and timing of future events at the time such statement was made. These forward‐looking statements are not a guarantee of our performance, and you should not place undue reliance on such statements. Forward looking statements may include statements about, among other things: our business strategy and the successful implementation of our business strategy; our future reserves; our financial strategy, liquidity and capital required for our development programs; estimated natural gas prices; our dividend policy; the timing and amount of future production of natural gas; our drilling and production plans; competition and government regulation; our ability to obtain and retain permits and governmental approvals; legal, regulatory or environmental matters; marketing of natural gas; business or leasehold acquisitions and integration of acquired businesses; our ability to develop our properties; the availability and cost of developing appropriate infrastructure around and transportation to our properties; the availability and cost of drilling rigs, production equipment, supplies, personnel and oilfield services; costs of developing our properties and of conducting our operations; our ability to reach FID and execute and complete our planned pipeline or planned LNG export projects; our anticipated Scope 1, Scope 2 and Scope 3 emissions from our businesses and our plans to offset our Scope 1, Scope 2 and Scope 3 emissions from our business; our ESG strategy and initiatives, including those relating to the generation and marketing of environmental attributes or new products seeking to benefit from ESG related activities; general economic conditions, including cost inflation; credit markets and the ability to obtain future financing on commercially acceptable terms; our ability to expand our business, including through the recruitment and retention of skilled personnel; our dependence on our key management personnel; our future operating results; and our plans, objectives, expectations and intentions. Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. Tamboran is subject to known and unknown risks, many of which are beyond the ability of Tamboran to control or predict. These risks may include, for example, movements in oil and gas prices, risks associated with the development and operation of the acreage, exchange rate fluctuations, an inability to obtain funding on acceptable terms or at all, loss of key personnel, an inability to obtain appropriate licenses, permits and or/or other approvals, inaccuracies in resource estimates, share market risks and changes in general economic conditions. Such risks may affect actual and future results of Tamboran and its securities. Maps and diagrams contained in this presentation are provided to assist with the identification and description of Tamboran’s interests. The maps and diagrams may not be drawn to scale. This presentation includes market data and other statistical information from third party sources, including independent industry publications, government publications or other published independent sources. Although we believe these third-party sources are reliable as of their respective dates, we have not independently verified the accuracy or completeness of this information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, which could cause our results to differ materially from those expressed in these third-party publications. Numbers in this report have been rounded. As a result, some figures may differ insignificantly due to rounding and totals reported may differ insignificantly from arithmetic addition of the rounded numbers. All currency amounts are represented as USD unless otherwise stated (AUD/USD exchange rate of 0.67). This presentation does not purport to be all inclusive or to necessarily contain all the information that you may need or desire to perform your analysis. In all cases, you should conduct your own investigation and analysis of the data set forth in this presentation, and should rely solely on your own judgment, review and analysis in evaluating this presentation. This presentation contains trademarks, tradenames and servicemarks of other companies that are the property of their respective owners. We do not intend our use or display of other companies’ trademarks, tradenames and servicemarks to imply relationships with, or endorsement or sponsorship of us by, these other companies. APA Group has not prepared, and was not responsible for the preparation of, this presentation. It does not make any statement contained in it and has not caused or authorised its release. To the maximum extent permitted by law, APA Group expressly disclaims any liability in connection with this presentation, and any statement contained in it. This announcement was approved and authorised for release by Mr. Joel Riddle, the Managing Director and Chief Executive Officer of Tamboran Resources Corporation. 2

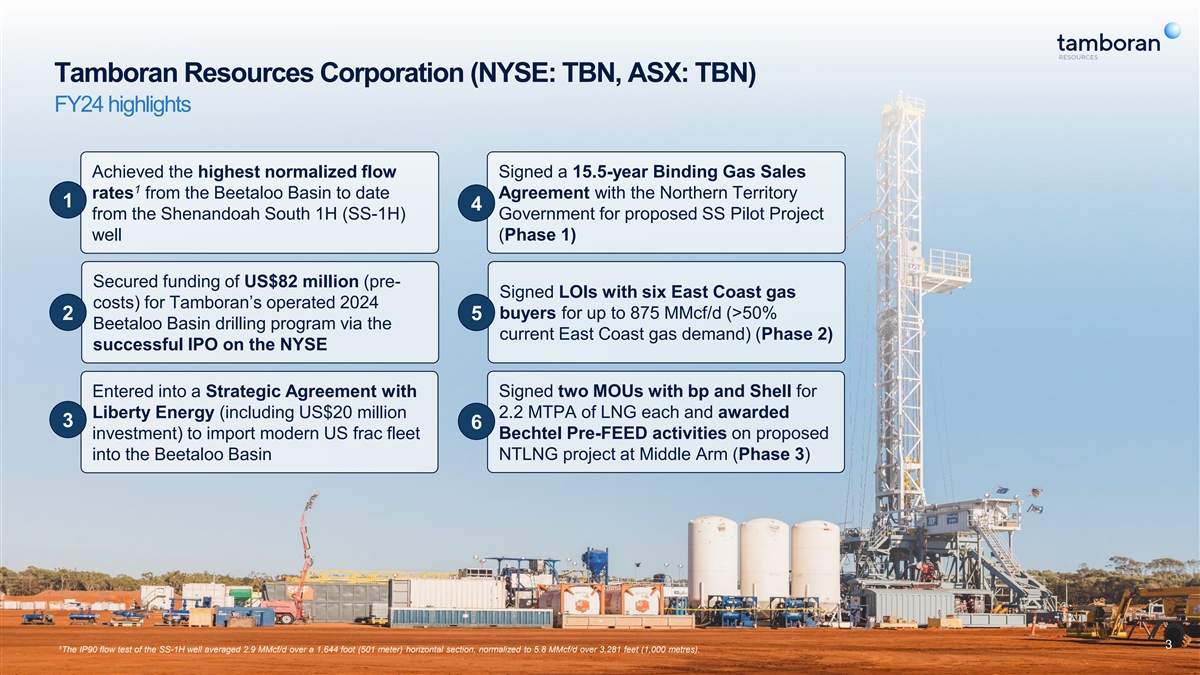

Tamboran Resources Corporation (NYSE: TBN, ASX: TBN) FY24 highlights Achieved the highest normalized flow Signed a 15.5-year Binding Gas Sales 1 rates from the Beetaloo Basin to date Agreement with the Northern Territory 1 4 from the Shenandoah South 1H (SS-1H) Government for proposed SS Pilot Project well (Phase 1) Secured funding of US$82 million (pre- Signed LOIs with six East Coast gas costs) for Tamboran’s operated 2024 buyers for up to 875 MMcf/d (>50% 2 5 Beetaloo Basin drilling program via the current East Coast gas demand) (Phase 2) successful IPO on the NYSE Entered into a Strategic Agreement with Signed two MOUs with bp and Shell for Liberty Energy (including US$20 million 2.2 MTPA of LNG each and awarded 3 6 investment) to import modern US frac fleet Bechtel Pre-FEED activities on proposed into the Beetaloo Basin NTLNG project at Middle Arm (Phase 3) 3 1 The IP90 flow test of the SS-1H well averaged 2.9 MMcf/d over a 1,644 foot (501 meter) horizontal section, normalized to 5.8 MMcf/d over 3,281 feet (1,000 metres).

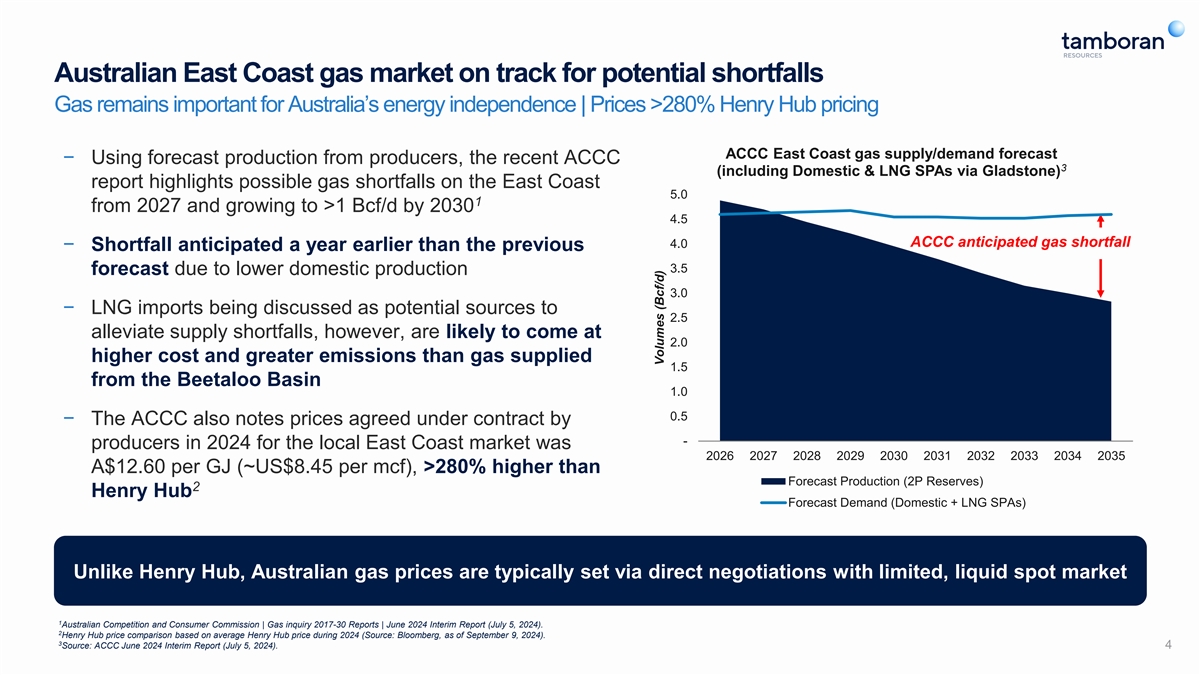

Australian East Coast gas market on track for potential shortfalls Gas remains important for Australia’s energy independence | Prices >280% Henry Hub pricing ACCC East Coast gas supply/demand forecast − Using forecast production from producers, the recent ACCC 3 (including Domestic & LNG SPAs via Gladstone) report highlights possible gas shortfalls on the East Coast 5.0 1 from 2027 and growing to >1 Bcf/d by 2030 4.5 4.0 ACCC anticipated gas shortfall − Shortfall anticipated a year earlier than the previous 3.5 forecast due to lower domestic production 3.0 − LNG imports being discussed as potential sources to 2.5 alleviate supply shortfalls, however, are likely to come at 2.0 higher cost and greater emissions than gas supplied 1.5 from the Beetaloo Basin 1.0 0.5 − The ACCC also notes prices agreed under contract by - producers in 2024 for the local East Coast market was 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 A$12.60 per GJ (~US$8.45 per mcf), >280% higher than Forecast Production (2P Reserves) 2 Henry Hub Forecast Demand (Domestic + LNG SPAs) Unlike Henry Hub, Australian gas prices are typically set via direct negotiations with limited, liquid spot market 1 Australian Competition and Consumer Commission | Gas inquiry 2017-30 Reports | June 2024 Interim Report (July 5, 2024). 2 Henry Hub price comparison based on average Henry Hub price during 2024 (Source: Bloomberg, as of September 9, 2024). 3 Source: ACCC June 2024 Interim Report (July 5, 2024). 4 Volumes (Bcf/d)

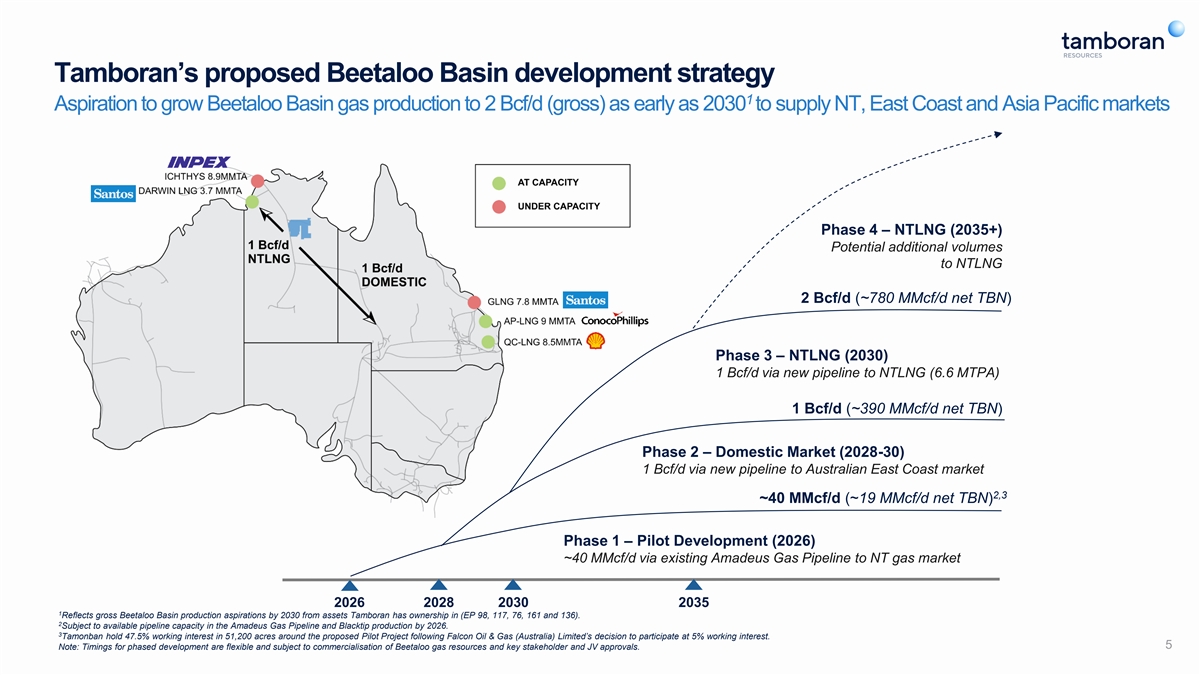

Tamboran’s proposed Beetaloo Basin development strategy 1 Aspiration to grow Beetaloo Basin gas production to 2 Bcf/d (gross) as early as 2030 to supply NT, East Coast and Asia Pacific markets Phase 4 – NTLNG (2035+) Potential additional volumes to NTLNG 2 Bcf/d (~780 MMcf/d net TBN) Phase 3 – NTLNG (2030) 1 Bcf/d via new pipeline to NTLNG (6.6 MTPA) 1 Bcf/d (~390 MMcf/d net TBN) Phase 2 – Domestic Market (2028-30) 1 Bcf/d via new pipeline to Australian East Coast market 2,3 ~40 MMcf/d (~19 MMcf/d net TBN) Phase 1 – Pilot Development (2026) ~40 MMcf/d via existing Amadeus Gas Pipeline to NT gas market 2026 2028 2030 2035 1 Reflects gross Beetaloo Basin production aspirations by 2030 from assets Tamboran has ownership in (EP 98, 117, 76, 161 and 136). 2 Subject to available pipeline capacity in the Amadeus Gas Pipeline and Blacktip production by 2026. 3 Tamonban hold 47.5% working interest in 51,200 acres around the proposed Pilot Project following Falcon Oil & Gas (Australia) Limited’s decision to participate at 5% working interest. 5 Note: Timings for phased development are flexible and subject to commercialisation of Beetaloo gas resources and key stakeholder and JV approvals.

Tamboran’s Strategic Partnerships in place to accelerate large scale Beetaloo and LNG development Delivering on commitment to import US technology and build additional pipelines into the Beetaloo Basin (7.2% TBN shareholder) (6.3% TBN shareholder) Strategic Drilling Partner Strategic Completions Partner Strategic Pipeline Partner LNG Pre-FEED EPC Contractor − Tamboran / H&P (NYSE: HP) − Tamboran and Liberty (NYSE: − Tamboran and APA Group (ASX: − Awarded Pre-FEED contract to Strategic Alliance to import LBRT) entered into Strategic APA) entered into three binding Bechtel, one of the world’s most modern US unconventional Partnership to import a modern agreements to support the experienced LNG EPC drilling rigs into the Beetaloo frac fleet into the Beetaloo Basin development of the Beetaloo contractors (commenced pre- Basin (currently operating) in 2024 (arrived 3Q 2024) Basin assets to the East Coast FEED) gas market and Darwin − Two-year rig contract in place for − Fit-for-purpose completion − Targeting completion of ® initial H&P FlexRig super-spec equipment has potential to − APA has agreed a process to NTLNG pre-FEED in 1H 2025 rig and an option to import four significantly reduce costs of continue development of the additional FlexRig super spec future completions and proposed pipelines with early rigs into the Beetaloo Basin increase efficiency works expenditure of up to A$10 million, subject to Tamboran reaching agreed milestones 6 6

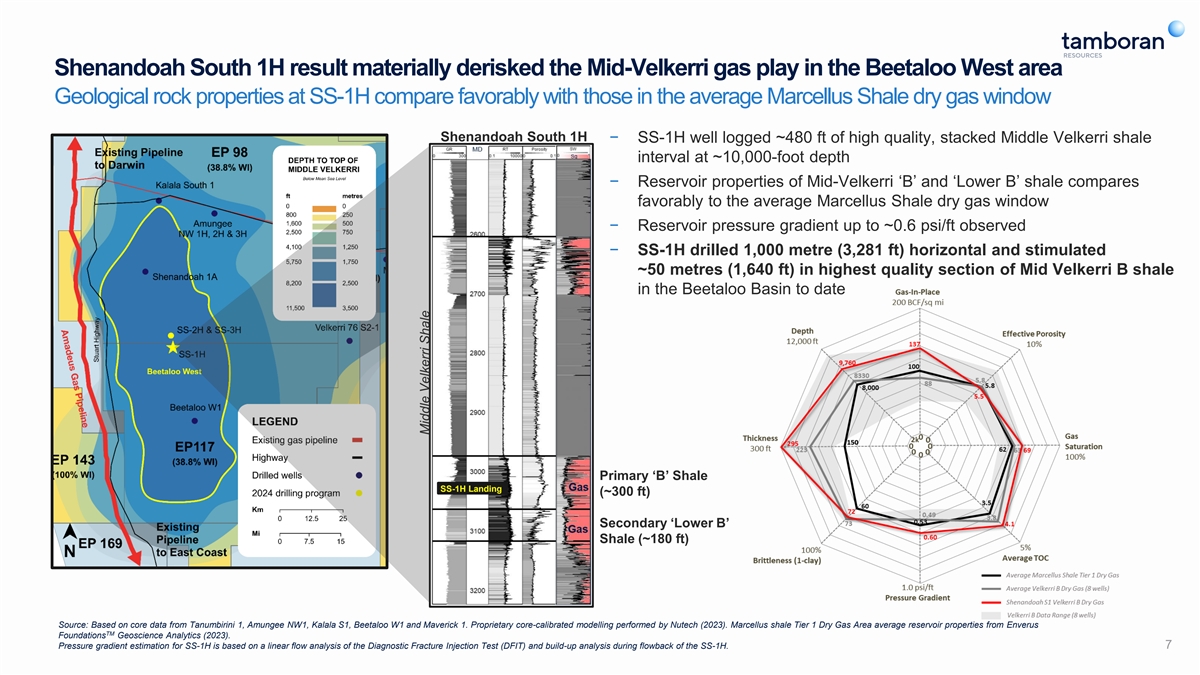

Shenandoah South 1H result materially derisked the Mid-Velkerri gas play in the Beetaloo West area Geological rock properties at SS-1H compare favorably with those in the average Marcellus Shale dry gas window Shenandoah South 1H − SS-1H well logged ~480 ft of high quality, stacked Middle Velkerri shale interval at ~10,000-foot depth − Reservoir properties of Mid-Velkerri ‘B’ and ‘Lower B’ shale compares favorably to the average Marcellus Shale dry gas window − Reservoir pressure gradient up to ~0.6 psi/ft observed − SS-1H drilled 1,000 metre (3,281 ft) horizontal and stimulated ~50 metres (1,640 ft) in highest quality section of Mid Velkerri B shale in the Beetaloo Basin to date Primary ‘B’ Shale SS-1H Landing (~300 ft) Secondary ‘Lower B’ Shale (~180 ft) Source: Based on core data from Tanumbirini 1, Amungee NW1, Kalala S1, Beetaloo W1 and Maverick 1. Proprietary core-calibrated modelling performed by Nutech (2023). Marcellus shale Tier 1 Dry Gas Area average reservoir properties from Enverus TM Foundations Geoscience Analytics (2023). Pressure gradient estimation for SS-1H is based on a linear flow analysis of the Diagnostic Fracture Injection Test (DFIT) and build-up analysis during flowback of the SS-1H. 7 Middle Velkerri Shale

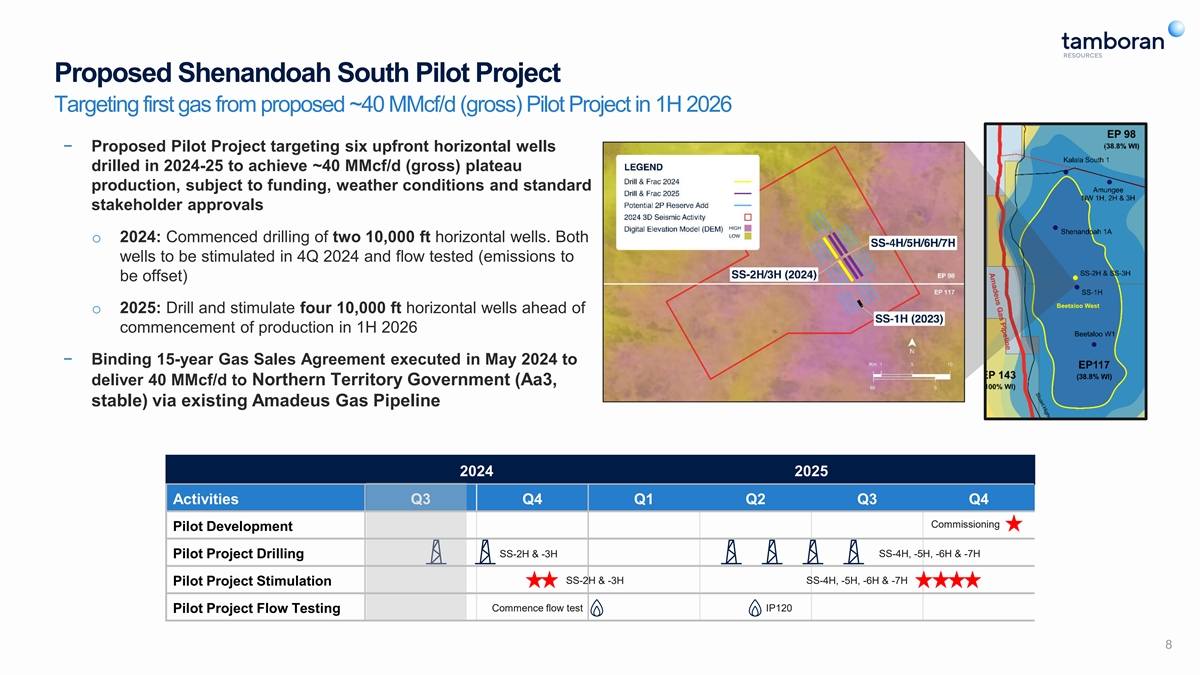

Proposed Shenandoah South Pilot Project Targeting first gas from proposed ~40 MMcf/d (gross) Pilot Project in 1H 2026 − Proposed Pilot Project targeting six upfront horizontal wells drilled in 2024-25 to achieve ~40 MMcf/d (gross) plateau production, subject to funding, weather conditions and standard stakeholder approvals o 2024: Commenced drilling of two 10,000 ft horizontal wells. Both wells to be stimulated in 4Q 2024 and flow tested (emissions to be offset) o 2025: Drill and stimulate four 10,000 ft horizontal wells ahead of commencement of production in 1H 2026 − Binding 15-year Gas Sales Agreement executed in May 2024 to deliver 40 MMcf/d to Northern Territory Government (Aa3, stable) via existing Amadeus Gas Pipeline 2024 2025 Activities Q3 Q4 Q1 Q2 Q3 Q4 Commissioning Pilot Development SS-2H & -3H SS-4H, -5H, -6H & -7H Pilot Project Drilling SS-2H & -3H SS-4H, -5H, -6H & -7H Pilot Project Stimulation Commence flow test IP120 Pilot Project Flow Testing 8

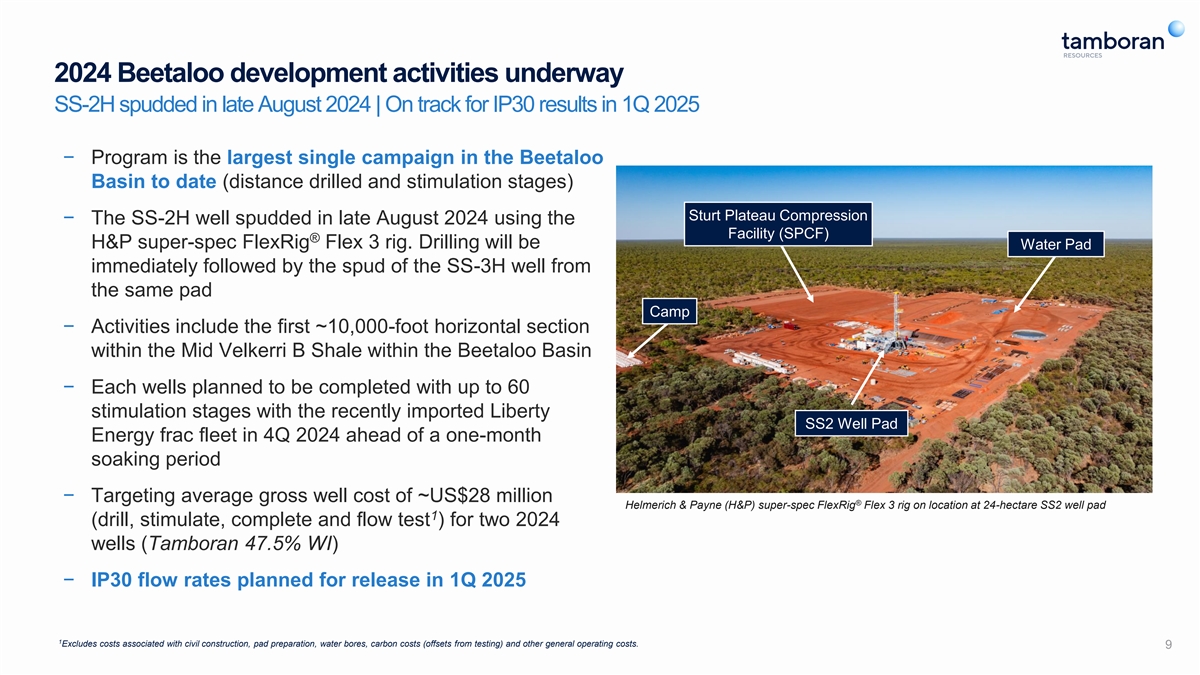

2024 Beetaloo development activities underway SS-2H spudded in late August 2024 | On track for IP30 results in 1Q 2025 − Program is the largest single campaign in the Beetaloo Basin to date (distance drilled and stimulation stages) Sturt Plateau Compression − The SS-2H well spudded in late August 2024 using the Facility (SPCF) ® H&P super-spec FlexRig Flex 3 rig. Drilling will be Water Pad immediately followed by the spud of the SS-3H well from the same pad Camp − Activities include the first ~10,000-foot horizontal section within the Mid Velkerri B Shale within the Beetaloo Basin − Each wells planned to be completed with up to 60 stimulation stages with the recently imported Liberty SS2 Well Pad Energy frac fleet in 4Q 2024 ahead of a one-month soaking period − Targeting average gross well cost of ~US$28 million ® Helmerich & Payne (H&P) super-spec FlexRig Flex 3 rig on location at 24-hectare SS2 well pad 1 (drill, stimulate, complete and flow test ) for two 2024 wells (Tamboran 47.5% WI) − IP30 flow rates planned for release in 1Q 2025 1 Excludes costs associated with civil construction, pad preparation, water bores, carbon costs (offsets from testing) and other general operating costs. 9

“US-style” Completion Design enabled by new Liberty Energy Frac Spread Liberty Energy 80,000 HP frac fleet imported from US into Australia for dedicated Beetaloo large scale development − The first 80,000 hydraulic horsepower (HHP) frac spread equipment imported into Australia from Liberty Energy arrived at the Port of Darwin and cleared customs − The frac feet is comprised of 32 pumps and auxiliary equipment, capable of delivering optimised stimulation of the Mid Velkerri B Shale − ~400 sand boxes have started to arrive at the SS2 well pad in the Liberty Energy frac spread being unloaded in Darwin, Northern Territory, Beetaloo Basin Australia − Equipment to be ready for stimulation of SS-2H and -3H wells in 4Q 2024 ahead of 1Q 2025 flow results 10

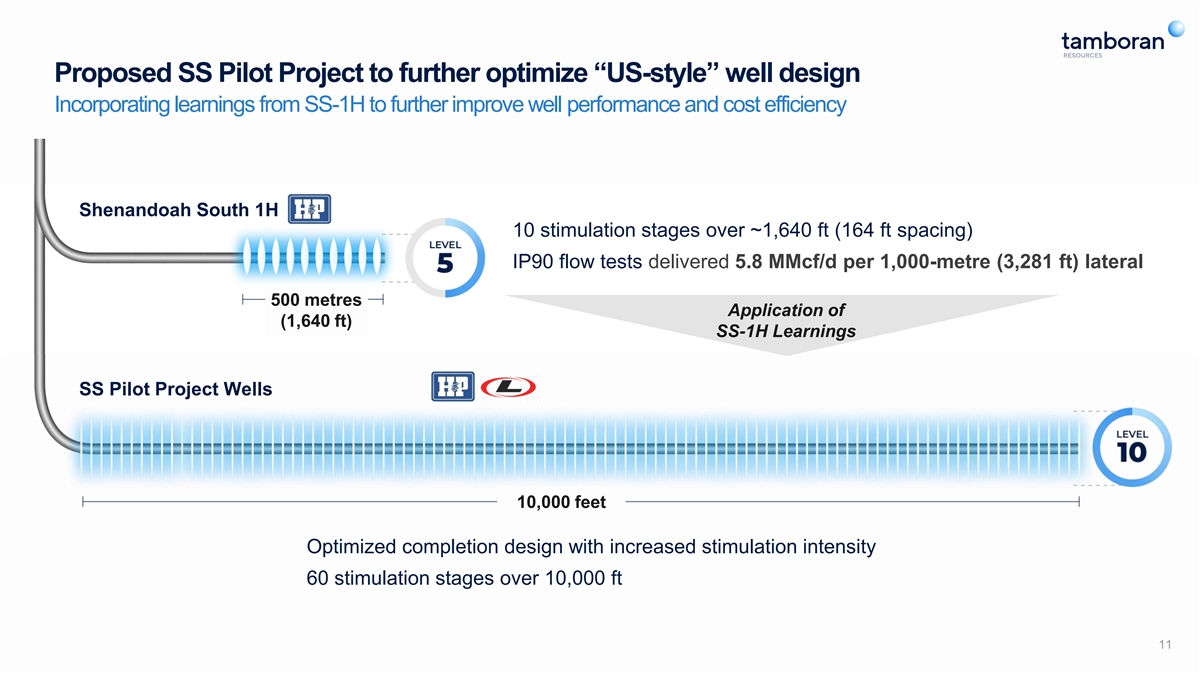

Proposed SS Pilot Project to further optimize “US-style” well design Incorporating learnings from SS-1H to further improve well performance and cost efficiency Shenandoah South 1H 10 stimulation stages over ~1,640 ft (164 ft spacing) Targeting ~5 mmscfd per 1,000-metre (3,280 feet) lateral IP90 flow tests delivered 5.8 MMcf/d per 1,000-metre (3,281 ft) lateral Planning ~10 stimulation stages 500 metres Application of (1,640 ft) SS-1H Learnings SS Pilot Project Wells 10,000 feet Optimized completion design with increased stimulation intensity 60 stimulation stages over 10,000 ft 11

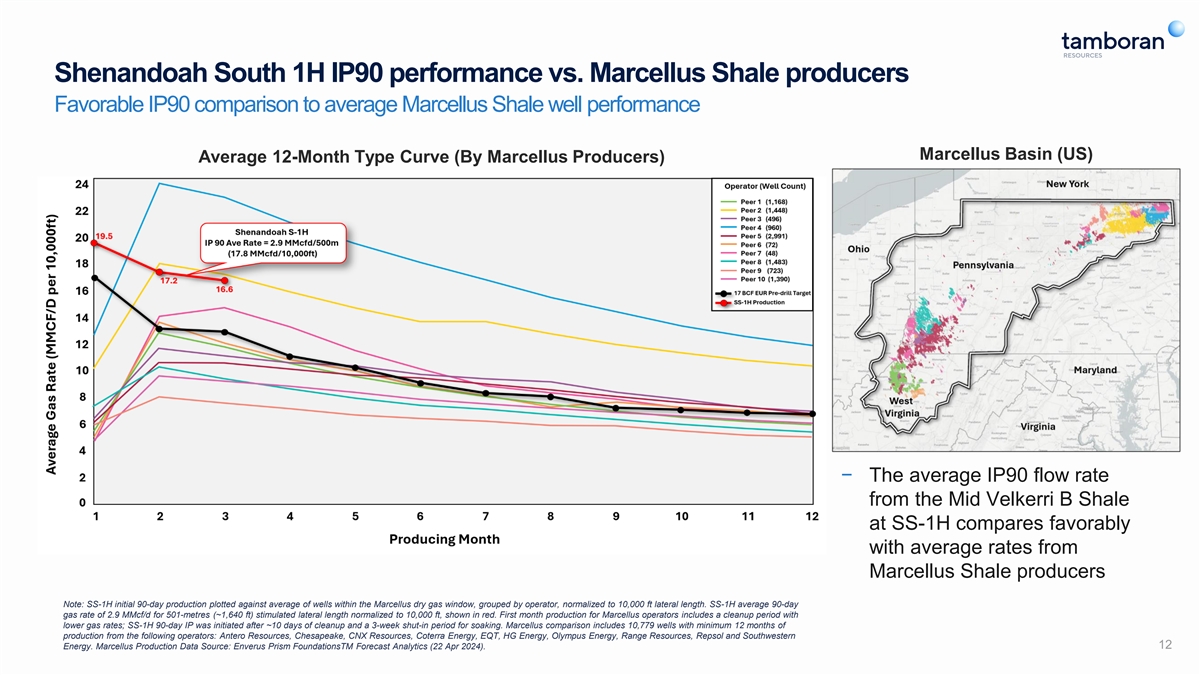

Shenandoah South 1H IP90 performance vs. Marcellus Shale producers Favorable IP90 comparison to average Marcellus Shale well performance Marcellus Basin (US) Average 12-Month Type Curve (By Marcellus Producers) − The average IP90 flow rate from the Mid Velkerri B Shale at SS-1H compares favorably with average rates from Marcellus Shale producers Note: SS-1H initial 90-day production plotted against average of wells within the Marcellus dry gas window, grouped by operator, normalized to 10,000 ft lateral length. SS-1H average 90-day gas rate of 2.9 MMcf/d for 501-metres (~1,640 ft) stimulated lateral length normalized to 10,000 ft, shown in red. First month production for Marcellus operators includes a cleanup period with lower gas rates; SS-1H 90-day IP was initiated after ~10 days of cleanup and a 3-week shut-in period for soaking. Marcellus comparison includes 10,779 wells with minimum 12 months of production from the following operators: Antero Resources, Chesapeake, CNX Resources, Coterra Energy, EQT, HG Energy, Olympus Energy, Range Resources, Repsol and Southwestern 12 Energy. Marcellus Production Data Source: Enverus Prism FoundationsTM Forecast Analytics (22 Apr 2024).

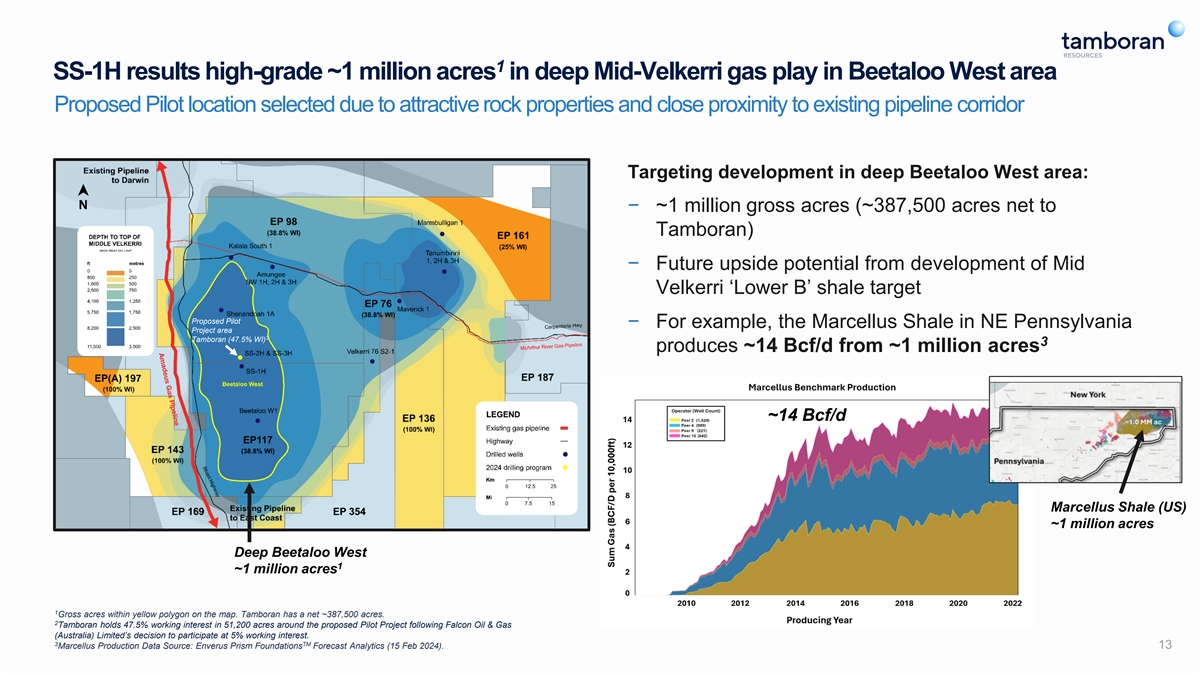

1 SS-1H results high-grade ~1 million acres in deep Mid-Velkerri gas play in Beetaloo West area Proposed Pilot location selected due to attractive rock properties and close proximity to existing pipeline corridor Targeting development in deep Beetaloo West area: − ~1 million gross acres (~387,500 acres net to Tamboran) − Future upside potential from development of Mid Velkerri ‘Lower B’ shale target Proposed Pilot − For example, the Marcellus Shale in NE Pennsylvania Project area 2 Tamboran (47.5% WI) 3 produces ~14 Bcf/d from ~1 million acres ~14 Bcf/d Marcellus Shale (US) ~1 million acres Deep Beetaloo West 1 ~1 million acres 1 Gross acres within yellow polygon on the map. Tamboran has a net ~387,500 acres. 2 Tamboran holds 47.5% working interest in 51,200 acres around the proposed Pilot Project following Falcon Oil & Gas (Australia) Limited’s decision to participate at 5% working interest. 3 TM Marcellus Production Data Source: Enverus Prism Foundations Forecast Analytics (15 Feb 2024). 13

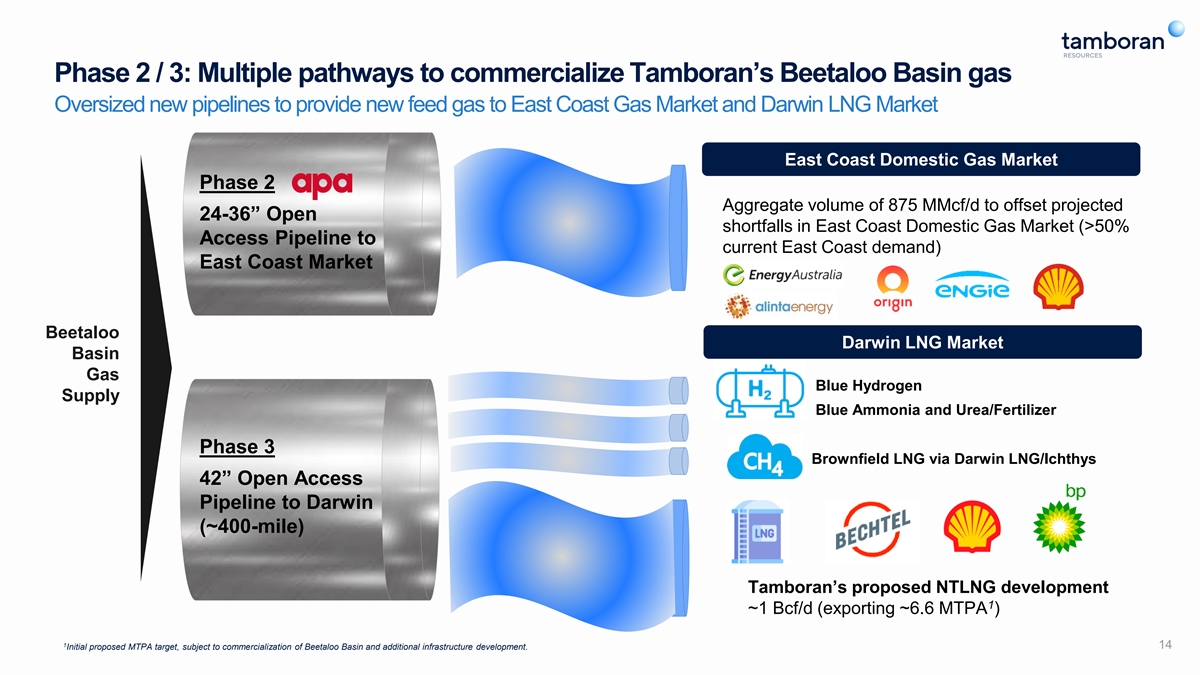

Phase 2 / 3: Multiple pathways to commercialize Tamboran’s Beetaloo Basin gas Oversized new pipelines to provide new feed gas to East Coast Gas Market and Darwin LNG Market East Coast Domestic Gas Market Phase 2 Aggregate volume of 875 MMcf/d to offset projected 24-36” Open shortfalls in East Coast Domestic Gas Market (>50% Access Pipeline to current East Coast demand) East Coast Market Beetaloo Darwin LNG Market Basin Gas Blue Hydrogen Supply Blue Ammonia and Urea/Fertilizer Phase 3 Brownfield LNG via Darwin LNG/Ichthys 42” Open Access Pipeline to Darwin (~400-mile) Tamboran’s proposed NTLNG development 1 ~1 Bcf/d (exporting ~6.6 MTPA ) 1 14 Initial proposed MTPA target, subject to commercialization of Beetaloo Basin and additional infrastructure development.

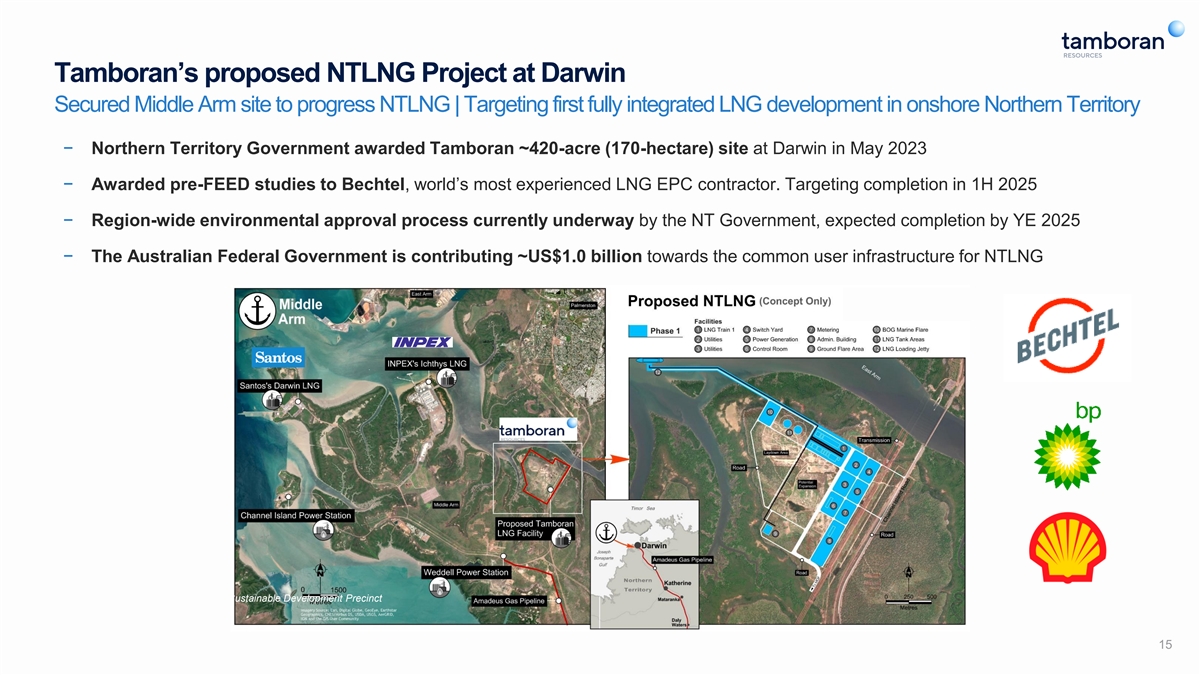

Tamboran’s proposed NTLNG Project at Darwin Secured Middle Arm site to progress NTLNG | Targeting first fully integrated LNG development in onshore Northern Territory − Northern Territory Government awarded Tamboran ~420-acre (170-hectare) site at Darwin in May 2023 − Awarded pre-FEED studies to Bechtel, world’s most experienced LNG EPC contractor. Targeting completion in 1H 2025 − Region-wide environmental approval process currently underway by the NT Government, expected completion by YE 2025 − The Australian Federal Government is contributing ~US$1.0 billion towards the common user infrastructure for NTLNG Ichthys LNG Project on Middle Arm Sustainable Development Precinct 15

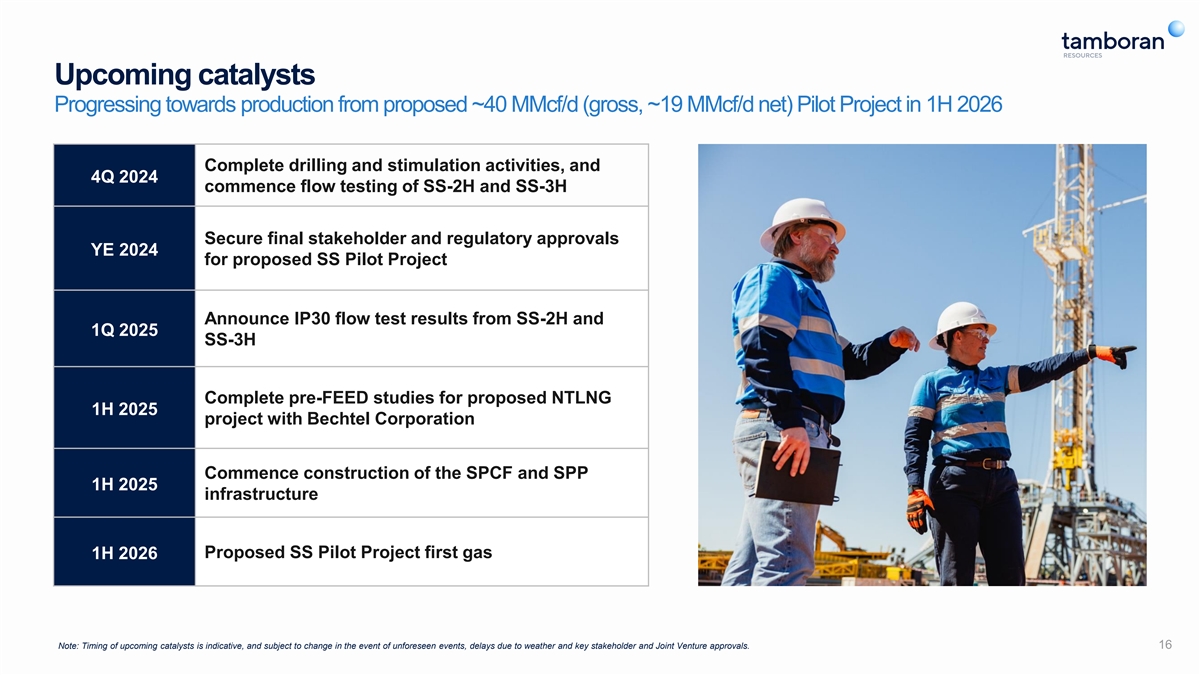

Upcoming catalysts Progressing towards production from proposed ~40 MMcf/d (gross, ~19 MMcf/d net) Pilot Project in 1H 2026 Complete drilling and stimulation activities, and 4Q 2024 commence flow testing of SS-2H and SS-3H Secure final stakeholder and regulatory approvals YE 2024 for proposed SS Pilot Project Announce IP30 flow test results from SS-2H and 1Q 2025 SS-3H Complete pre-FEED studies for proposed NTLNG 1H 2025 project with Bechtel Corporation Commence construction of the SPCF and SPP 1H 2025 infrastructure 1H 2026 Proposed SS Pilot Project first gas Note: Timing of upcoming catalysts is indicative, and subject to change in the event of unforeseen events, delays due to weather and key stakeholder and Joint Venture approvals. 16